Lecture 6 - Bayesian Binary Logistic Regression#

Today’s Learning Objectives#

Extend the paradigm of Bayesian regression to Generalized Linear Models (GLMs), specifically Binary Logistic regression.

Explore and contrast Bayesian Binary Logistic regression versus its frequentist counterpart.

Illustrate the Bayesian modelling setup in Binary Logistic regression.

Compare the Bayesian prior and posterior sigmoid curves in simple Binary Logistic regression.

Compare the Bayesian prior and posterior predicted probabilities in simple Binary Logistic regression.

Loading R Packages#

options(repr.matrix.max.rows = 6)

library(bayesrules)

library(tidyverse)

library(broom)

library(rstan)

library(bayesplot)

library(broom.mixed)

library(cowplot)

library(janitor)

library(wesanderson)

Previously…#

We introduced Bayesian Normal regression, comparable to Ordinary Least-Squares (OLS). Nonetheless, we tweaked the frequentist concepts to a Bayesian framework. For instance, we do not use \(p\)-values in a Bayesian framework to perform inference. Nevertheless, we can use posterior credible intervals to test whether a given regression coefficient is different from zero (i.e., whether the credible interval contains zero or not).

Furthermore, we know there are more regression models besides the classical OLS. As we saw in DSCI 562, we will encounter different types of responses. Hence, there is always a specific regression model for each possible case. Recall GLMs, such as Binary Logistic regression, are estimated via maximum likelihood.

{kind=link}

GLMs also have a Bayesian version, and we can obtain an approximate posterior for the regression parameters via Markov Chain Monte Carlo (MCMC)!

1. Cards Against Humanity’s “Pulse of the Nation” Survey#

We will use the dataset pulse_of_the_nation found in the package bayesrules to contrast Bayesian Binary Logistic regression versus its frequentist counterpart.

According to the package’s documentation, the description is the following:

Cards Against Humanity’s “Pulse of the Nation” project (https://thepulseofthenation.com/) conducted monthly polls into people’s social and political views, as well as some silly things. This data includes responses to a subset of questions included in the poll conducted in September 2017.

The dataset contains \(n = 1000\) observations (i.e., surveyed subjects) and fifteen variables.

pulse_of_the_nation

| income | age | party | trump_approval | education | robots | climate_change | transformers | science_is_honest | vaccines_are_safe | books | ghosts | fed_sci_budget | earth_sun | wise_unwise |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <fct> | <fct> | <fct> | <fct> | <fct> | <dbl> | <fct> | <fct> | <dbl> | <fct> | <fct> | <lgl> | <fct> |

| 8 | 64 | Democrat | Strongly disapprove | College degree | Unlikely | Real and Caused by People | 1 | Strongly Agree | Somewhat Disagree | 20 | Yes | Too Low | FALSE | Wise but Unhappy |

| 68 | 56 | Democrat | Strongly disapprove | High school | Unlikely | Real and Caused by People | 0 | Somewhat Agree | Somewhat Disagree | 6 | No | Too High | FALSE | Wise but Unhappy |

| 46 | 63 | Independent | Somewhat Approve | Some college | Unlikely | Real but not Caused by People | 0 | Somewhat Agree | Strongly Agree | 0 | No | About Right | TRUE | Happy but Unwise |

| ⋮ | ⋮ | ⋮ | ⋮ | ⋮ | ⋮ | ⋮ | ⋮ | ⋮ | ⋮ | ⋮ | ⋮ | ⋮ | ⋮ | ⋮ |

| 70 | 74 | Republican | Strongly Approve | Some college | Unlikely | Real and Caused by People | 0 | Somewhat Agree | Neither Agree nor Disagree | 3 | No | Too High | FALSE | Wise but Unhappy |

| 93 | 60 | Independent | Strongly disapprove | Graduate degree | Unlikely | Real but not Caused by People | 0 | Somewhat Disagree | Strongly Agree | 4 | Yes | Too Low | TRUE | Happy but Unwise |

| 35 | 46 | Independent | Strongly Approve | High school | Likely | Not Real At All | 3 | Strongly Agree | Strongly Agree | 0 | No | About Right | TRUE | Happy but Unwise |

We are interested in the following variables:

income: Subject’s annual income in thousand USD. It is a continuous variable.climate_change: Subject’s belief in climate change. It is a categorical variable with three levels (Not Real At All,Real and Caused by People,Real but not Caused by People,).

pulse_training <- pulse_of_the_nation |>

select(income, climate_change)

pulse_training

levels(pulse_training$climate_change)

| income | climate_change |

|---|---|

| <dbl> | <fct> |

| 8 | Real and Caused by People |

| 68 | Real and Caused by People |

| 46 | Real but not Caused by People |

| ⋮ | ⋮ |

| 70 | Real and Caused by People |

| 93 | Real but not Caused by People |

| 35 | Not Real At All |

- 'Not Real At All'

- 'Real and Caused by People'

- 'Real but not Caused by People'

Main statistical inquiries

Suppose we are interested in the following statistical inquiries:

How is continuous

incomeassociated withclimate_change?Is there a numerical result that can quantify this association?

Exercise 17

We will view climate_change as our response of interest and income as our feature. Thus, regression analysis will help you address these inquiries. Now, the question is: what regression model should we use via a frequentist approach??

A. A generalized linear model (GLM) such as Multinomial regression.

B. A GLM such as Ordinal Logistic regression.

C. A GLM such as Poisson regression.

D. Ordinary Least-squares (OLS).

We need to start with a simple approach as a Bayesian GLM. Therefore, let us convert climate_change to a binary response: 1 for Real and Caused by People and Real but not Caused by People, along with 0 for Not Real At All.

levels(pulse_training$climate_change)

- 'Not Real At All'

- 'Real and Caused by People'

- 'Real but not Caused by People'

pulse_training <- pulse_training |>

mutate(climate_change = case_when(

climate_change == "Real and Caused by People" ~ 1,

climate_change == "Real but not Caused by People" ~ 1,

climate_change == "Not Real At All" ~ 0

))

pulse_training

| income | climate_change |

|---|---|

| <dbl> | <dbl> |

| 8 | 1 |

| 68 | 1 |

| 46 | 1 |

| ⋮ | ⋮ |

| 70 | 1 |

| 93 | 1 |

| 35 | 0 |

2. Exploratory Data Analysis#

Let us make a quick exploratory data analysis on pulse_training for climate_change versus income via side-by-side boxplots. Moreover, note 15% of the respondents believe climate change is not real!

pulse_training |>

tabyl(climate_change) |>

adorn_pct_formatting()

| climate_change | n | percent |

|---|---|---|

| <dbl> | <dbl> | <chr> |

| 0 | 150 | 15.0% |

| 1 | 850 | 85.0% |

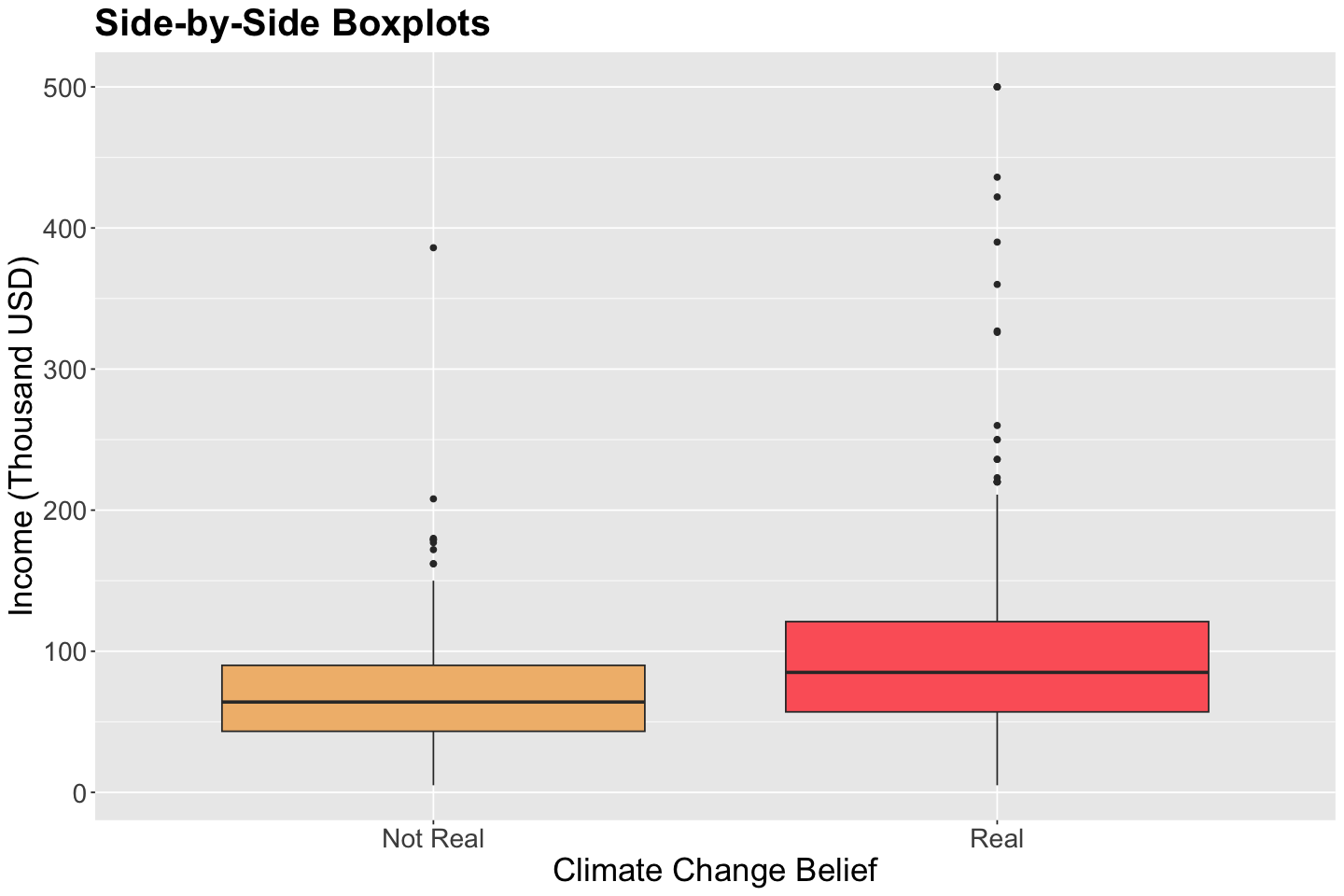

The below side-by-side boxplots show graphical evidence for lower incomes leaning more to the category Not Real in climate_change.

options(repr.plot.height = 8, repr.plot.width = 12)

climate_change_boxplots <- pulse_training |>

ggplot(aes(as.factor(climate_change), income)) +

geom_boxplot(aes(fill = as.factor(climate_change))) +

labs(y = "Income (Thousand USD)", x = "Climate Change Belief") +

ggtitle("Side-by-Side Boxplots") +

theme(

plot.title = element_text(size = 24, face = "bold"),

axis.text = element_text(size = 17),

axis.title = element_text(size = 21),

legend.position = "none"

) +

scale_x_discrete(labels=c("0" = "Not Real", "1" = "Real")) +

scale_fill_manual(values = wes_palette(n = 3, name = "GrandBudapest1"))

climate_change_boxplots

3. Frequentist Logistic Regression#

Let us review the frequentist Binary Logistic regression. For \(i = 1, \dots, n\) (where \(n\) is the training size) its response variable has the form:

As the response variable can only take the values \(0\) or \(1\), the key modelling term becomes the probability that \(Y_i\) takes on the value of \(1\), i.e. the probability of success, denoted as \(\pi_i\). Hence:

Specifically, \(\pi_i\) (\(i = 1, 2, \dots, n\)) will depend on the values of the \(k\) regressors \(X_{i, 1}, X_{i, 2}, \dots, X_{i, k}\) in the form:

or equivalently

The log of the odds \(\log \bigg( \frac{\pi_i}{1 - \pi_i}\bigg) \) is the link function in this GLM, i.e., the logarithm of the ratio of the probability of the event to the probability of the non-event.

In this example, let:

and \(X_{i,\text{income}}\) our single regressor.

Hence, the model becomes:

Note we have two regression parameters: \(\beta_0\) and \(\beta_1\). These parameters will be unrestricted on the real scale.

Firstly, we run a frequentist Binary Logistic regression via glm() (i.e., using maximum likelihood estimation). Note the following:

incomeis statistically significant for the log of the odds.The interpretation for \(\hat{\beta}_1\) is: “for each one thousand USD increase in

income, a subject is 1.009 times more likely to believe in climate change than not to”.

freq_log_reg <- glm(climate_change ~ income, data = pulse_training, family = "binomial")

summary_freq_log_reg <- tidy(freq_log_reg, conf.int = TRUE) |>

mutate(

exp.estimate = exp(estimate),

exp.conf.low = exp(conf.low),

exp.conf.high = exp(conf.high)

) %>%

mutate_if(is.numeric, round, 3)

summary_freq_log_reg

| term | estimate | std.error | statistic | p.value | conf.low | conf.high | exp.estimate | exp.conf.low | exp.conf.high |

|---|---|---|---|---|---|---|---|---|---|

| <chr> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> |

| (Intercept) | 0.965 | 0.184 | 5.248 | 0 | 0.606 | 1.327 | 2.625 | 1.834 | 3.771 |

| income | 0.009 | 0.002 | 4.376 | 0 | 0.005 | 0.014 | 1.009 | 1.005 | 1.014 |

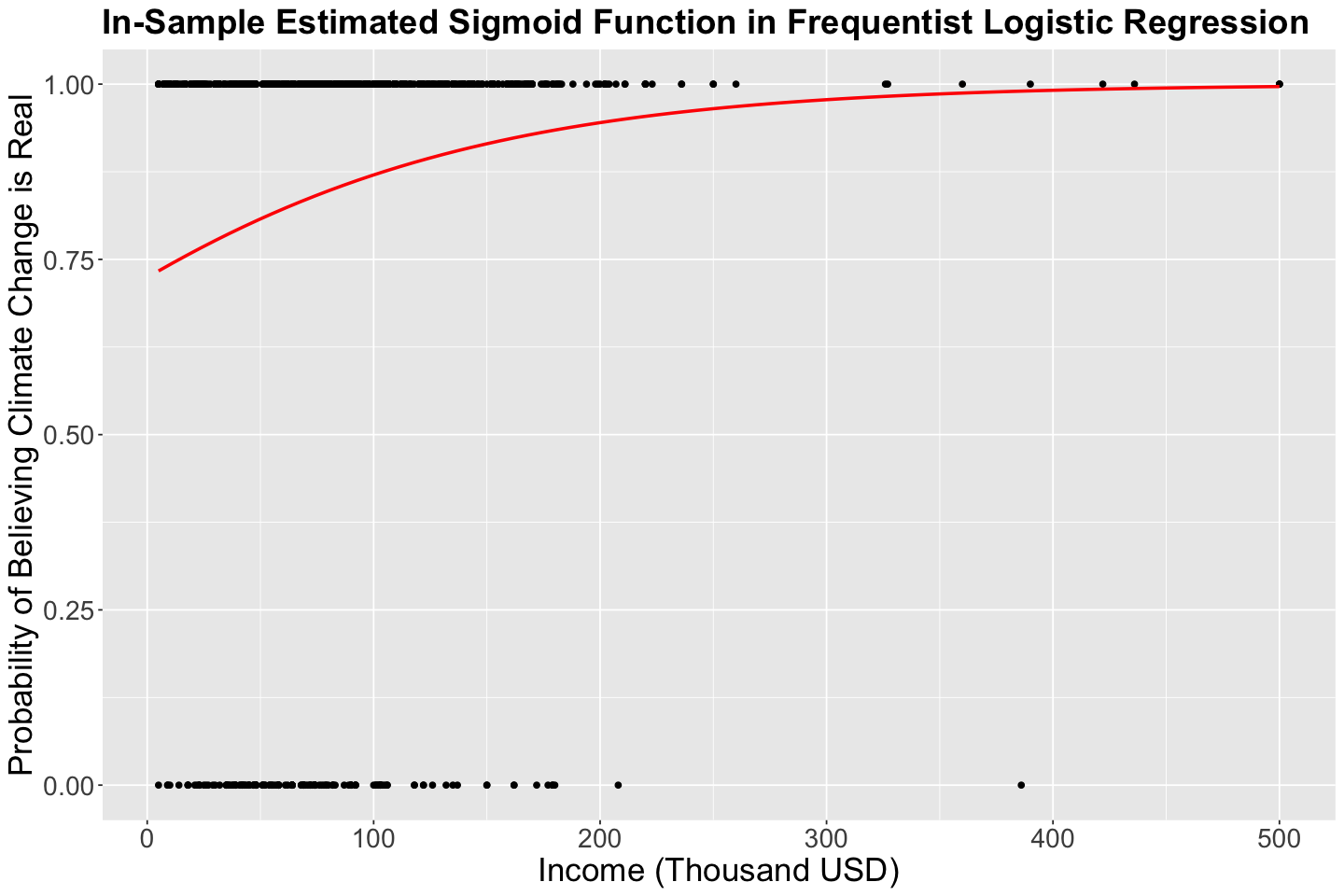

The log of the odds can be put on the probability scale as follows:

This is the sigmoid function. The in-sample \(\hat{\pi}_i\) values are shown below. There is no \(S\)-shaped in this case given the values for \(\hat{\beta}_0\) and \(\hat{\beta}_1\)

plot_freq_log_reg <- pulse_training |>

ggplot() +

geom_point(aes(income, climate_change)) +

geom_smooth(aes(income, climate_change),

method = "glm", method.args = c(family = binomial), formula = "y ~ x", se = FALSE, color = "red") +

labs(y = "Probability of Believing Climate Change is Real", x = "Income (Thousand USD)") +

ggtitle("In-Sample Estimated Sigmoid Function in Frequentist Logistic Regression") +

theme(

plot.title = element_text(size = 22, face = "bold"),

axis.text = element_text(size = 17),

axis.title = element_text(size = 21)

)

plot_freq_log_reg

4. Bayesian Logistic Regression#

4.1. The Likelihood#

Let us start our Bayesian model. First off, our respose will be assumed as:

We need to set up the systematic component of the model. Thus, we will use the link function:

This will be our likelihood:

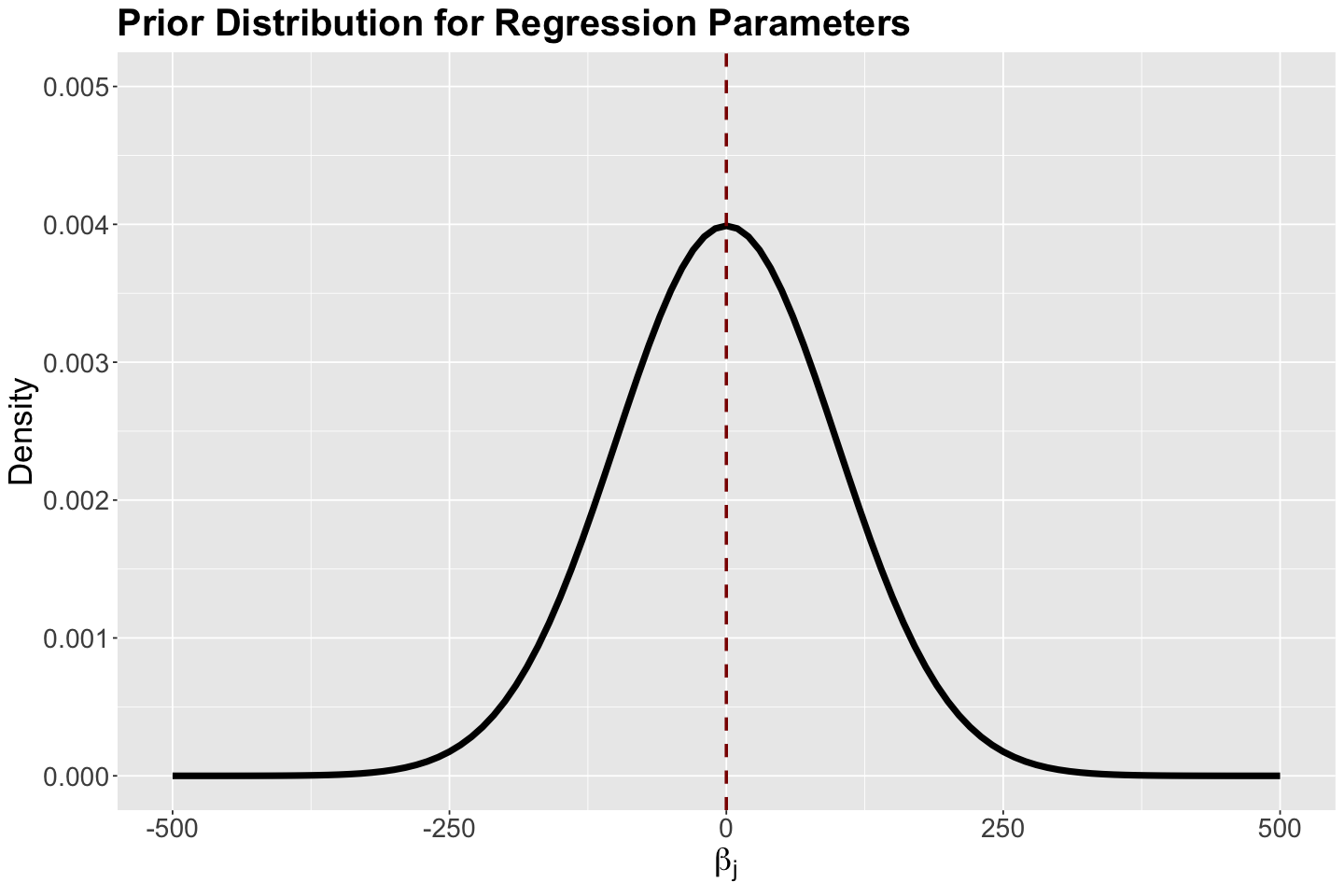

4.2. The Priors#

Unlike OLS, we do not have \(\sigma^2\). Therefore, our parameters of interest are \(\beta_0\) and \(\beta_1\). For the prior specification, we will proceed as follows:

\(\beta_0 \sim \mathcal{N}(\mu_{\beta_0} = 0, \sigma_{\beta_0}^2 = 100^2)\).

\(\beta_1 \sim \mathcal{N}(\mu_{\beta_1} = 0, \sigma_{\beta_1}^2 = 100^2)\).

We have to stress that for these prior specifications, we assume the prior mean of \(\beta_1\) as \(0\), since we do not know if the variable \(X_{i,\text{income}}\) has any association with \(Y_i\). On the other hand, the intercept \(\beta_0\) will be assumed as zero in our prior knowledge. We will use a large variances (i.e, \(\sigma_{\beta_j}^2 = 100^2\) for \(j = 0, 1\)) to reflect uncertainty.

The density plot for these priors is shown below with the corresponding hyperparameter mean (equal to zero) indicated as red vertical dashed line.

# Plotting Normal prior for regression parameters

prior_gamma_beta_j <- ggplot() +

xlim(-500, 500) +

ylim(0, 0.005) +

geom_function(fun = dnorm, args = list(mean = 0, sd = 100), linewidth = 2) +

theme(

plot.title = element_text(size = 24, face = "bold"),

axis.text.x = element_text(size = 17, angle = 0),

axis.text.y = element_text(size = 17, angle = 0),

axis.title = element_text(size = 21),

) +

labs(y = "Density", x = expression(beta["j"])) +

ggtitle("Prior Distribution for Regression Parameters") +

geom_vline(xintercept = 0, colour = "darkred", linetype = "dashed", linewidth = 1)

prior_gamma_beta_j

4.3. Coding a Prior Bayesian Model on Stan#

Before setting up our full Bayesian model, we will check why our likelihood (i.e., collected data) is essential. Suppose you set up a prior Bayesian model, i.e., you only code the prior distributions for \(\beta_0\) and \(\beta_1\) in Stan.

What does this mean? It means that we build a Stan code with the prior distribution of the parameters without specifying the likelihood and data block. Hence, the process becomes a Monte Carlo simulation in which we draw random values from the two prior normal distributions.

Caution

This is not MCMC since we are not applying the Bayes’ rule.

prior_stan_climate_change <- "parameters {

real beta_0;

real beta_1;

}

model {

beta_0 ~ normal(0, 100);

beta_1 ~ normal(0, 100);

}"

Therefore, when using the function stan() (or sampling() if we are using the R markdown), using thin and warmup might not be necessary. Furthermore, you do not need a data dictionary in this prior model.

prior_climate <- stan(

model_code = prior_stan_climate_change,

chains = 1,

iter = 1000,

warmup = 0,

thin = 1,

seed = 553

)

SAMPLING FOR MODEL 'anon_model' NOW (CHAIN 1).

Chain 1:

Chain 1: Gradient evaluation took 3e-06 seconds

Chain 1: 1000 transitions using 10 leapfrog steps per transition would take 0.03 seconds.

Chain 1: Adjust your expectations accordingly!

Chain 1:

Chain 1:

Chain 1: WARNING: No variance estimation is

Chain 1: performed for num_warmup < 20

Chain 1:

Chain 1: Iteration: 1 / 1000 [ 0%] (Sampling)

Chain 1: Iteration: 100 / 1000 [ 10%] (Sampling)

Chain 1: Iteration: 200 / 1000 [ 20%] (Sampling)

Chain 1: Iteration: 300 / 1000 [ 30%] (Sampling)

Chain 1: Iteration: 400 / 1000 [ 40%] (Sampling)

Chain 1: Iteration: 500 / 1000 [ 50%] (Sampling)

Chain 1: Iteration: 600 / 1000 [ 60%] (Sampling)

Chain 1: Iteration: 700 / 1000 [ 70%] (Sampling)

Chain 1: Iteration: 800 / 1000 [ 80%] (Sampling)

Chain 1: Iteration: 900 / 1000 [ 90%] (Sampling)

Chain 1: Iteration: 1000 / 1000 [100%] (Sampling)

Chain 1:

Chain 1: Elapsed Time: 0 seconds (Warm-up)

Chain 1: 0.13 seconds (Sampling)

Chain 1: 0.13 seconds (Total)

Chain 1:

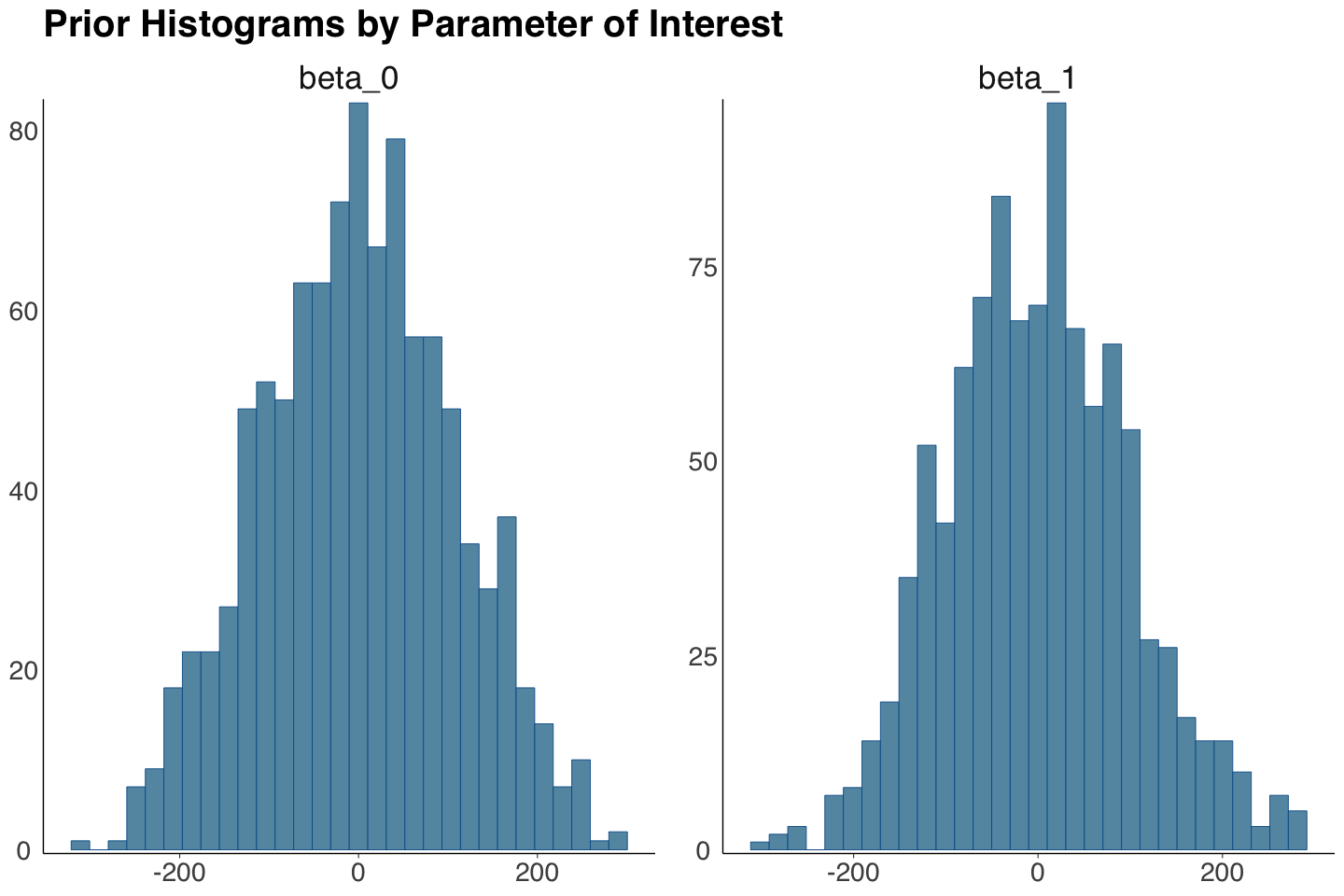

The output prior_climate will contain the prior samples for \(\beta_0\) and \(\beta_1\). Note the summary statistics are close to the hyperparameters we set up in prior_stan_climate_change.

prior_climate_samples <- as.data.frame(round(summary(prior_climate)$summary, 3))

prior_climate_samples <- prior_climate_samples[, c("mean", "sd")]

prior_climate_samples[1:2,]

| mean | sd | |

|---|---|---|

| <dbl> | <dbl> | |

| beta_0 | 0.732 | 108.576 |

| beta_1 | -0.062 | 99.967 |

We plot the prior histograms for these samples via mcmc_hist() from bayesplot. The distributions are symmetric and centred around zero.

prior_plots_betas <- mcmc_hist(prior_climate, pars = c("beta_0", "beta_1")) +

theme(

plot.title = element_text(size = 24, face = "bold", family = "sans"),

axis.text.x = element_text(size = 17, family = "sans"),

axis.text.y = element_text(size = 17, family = "sans"),

strip.text.x = element_text(size = 21, family = "sans")

) +

ggtitle("Prior Histograms by Parameter of Interest")

prior_plots_betas

`stat_bin()` using `bins = 30`. Pick better value with `binwidth`.

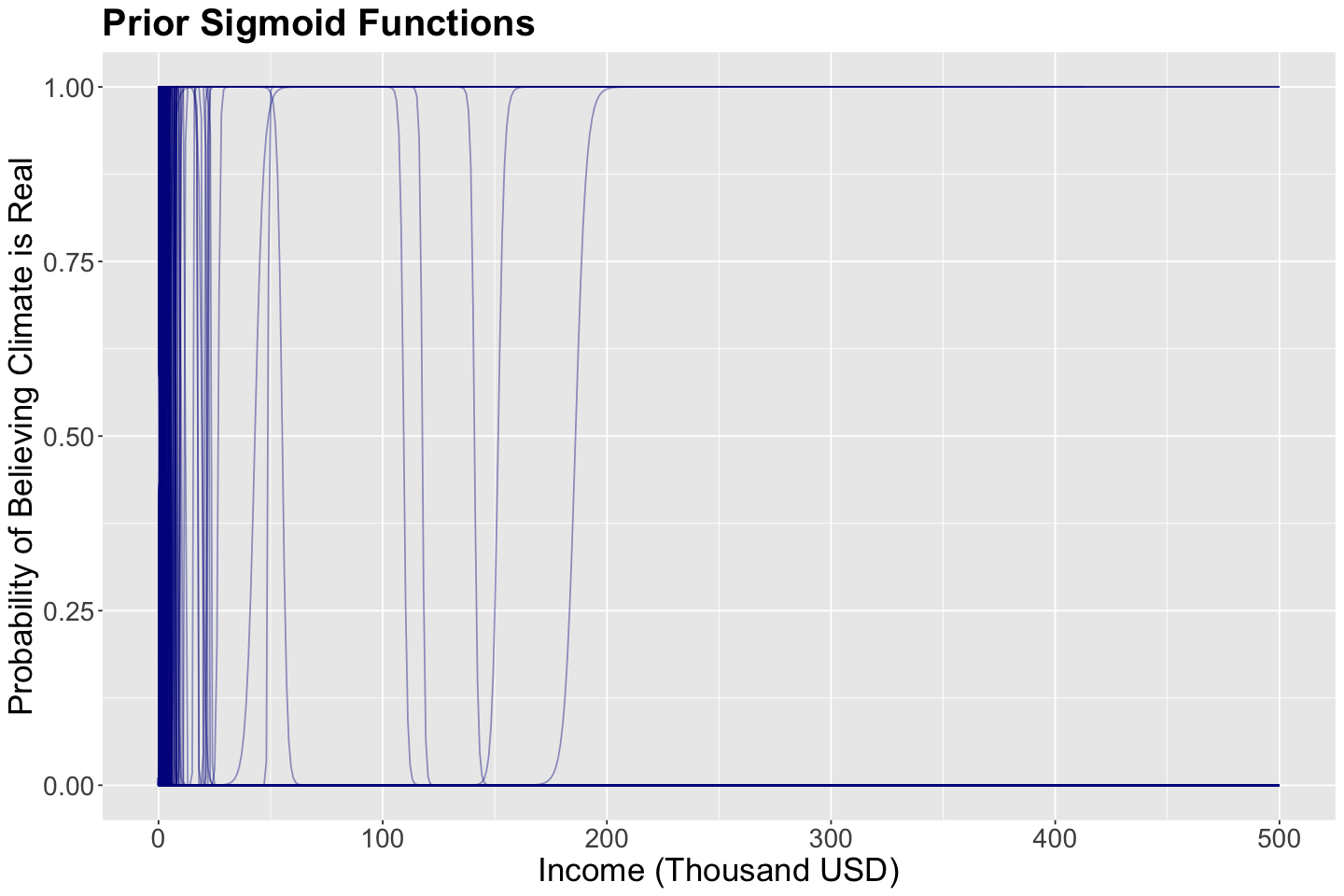

What is the purpose of getting these prior samples? These 1000 samples (pairs containing \(\beta_0\) and \(\beta_1\)) will be use to plot 1000 different sigmoid functions:

The regressor income is set up as a grid from 0 to 500 thousand USD to plot these 1000 sigmoid functions.

prior_climate <- as.data.frame(prior_climate) # prior_climate as data frame

income <- seq(0, 500, length.out = 500) # Setting up grid for income

beta_0 <- as.numeric(prior_climate[1, "beta_0"]) # First sample

beta_1 <- as.numeric(prior_climate[1, "beta_1"]) # First sample

logistic_like <- data.frame(income = income) |> # Computing probabilities with first sample

mutate(values = exp(beta_0 + beta_1 * income) / (1 + exp(beta_0 + beta_1 * income)))

plot_logistic_like_prior_stanfit <- ggplot(data = logistic_like, na.rm = TRUE) +

geom_line(aes(x = income, y = values), alpha = 0.1, color = "darkblue", na.rm = TRUE) +

labs(y = "Probability of Believing Climate is Real", x = "Income (Thousand USD)") +

ggtitle("Prior Sigmoid Functions") +

theme(

plot.title = element_text(size = 24, face = "bold"),

axis.text = element_text(size = 17),

axis.title = element_text(size = 21)

) # First ggplot layer

for (j in 2:nrow(prior_climate)) # Loop from the second sample to the last sample in prior_climate

{

beta_0 <- as.numeric(prior_climate[j, "beta_0"])

beta_1 <- as.numeric(prior_climate[j, "beta_1"])

logistic_like <- data.frame(income = income) |>

mutate(values = exp(beta_0 + beta_1 * income) / (1 + exp(beta_0 + beta_1 * income)))

plot_logistic_like_prior_stanfit <- plot_logistic_like_prior_stanfit +

geom_line(data = logistic_like, aes(x = income, y = values),

alpha = 0.4, color = "darkblue", na.rm = TRUE) # Next ggplot layer

}

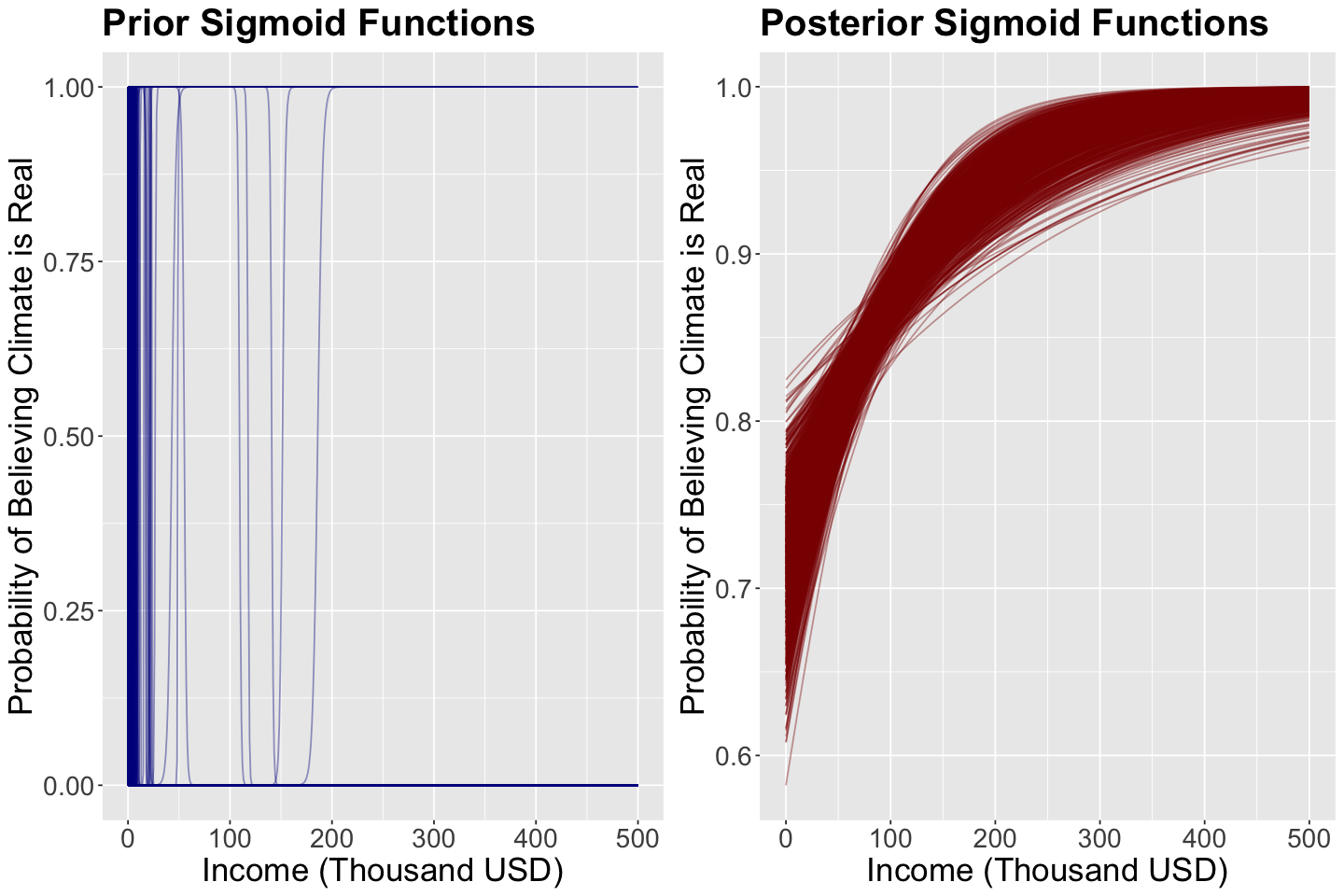

The plot below shows these 1000 sigmoid functions. We can think of this as a prior distribution over curves (since a curve is defined by \(\beta_0\) and \(\beta_1\)). Hence, these blue sigmoid curves are samples from this distribution.

plot_logistic_like_prior_stanfit

Exercise 18

Having explained all this prior model, do you see a clear distribution on these fitted curves?

A. Yes.

B. No.

4.4. Coding the Posterior Bayesian Model on Stan#

The full formal Bayesian logistic model is set up as follows:

Now, we will build a complete posterior_stan_climate_change with a data block and a likelihood in our model block. The vector for the response variable climate_change is set up as integer-type with lower and upper bounds.

Moreover we introduce a new modelling function bernoulli_logit(). This will indicate our logit function.

posterior_stan_climate_change <- "data {

int<lower=0> n; // number of observations

vector[n] income; // regressor income

int<lower=0,upper=1> climate_change[n]; // setting the response variable as binary

}

parameters {

real beta_0;

real beta_1;

}

model {

beta_0 ~ normal(0, 100);

beta_1 ~ normal(0, 100);

climate_change ~ bernoulli_logit(beta_0 + beta_1 * income);

}"

Since we have a data block in posterior_stan_climate_change, we need a climate_dictionary as the one below.

climate_dictionary <- list(

n = nrow(pulse_training),

income = pulse_training$income,

climate_change = as.integer(pulse_training$climate_change)

)

Finally, we run an MCMC simulation with posterior_stan_climate_change and climate_dictionary. This time we use appropriate values for iter, warmup, and thin.

posterior_climate <- stan(

model_code = posterior_stan_climate_change,

data = climate_dictionary,

chains = 1,

iter = 21000,

warmup = 1000,

thin = 20,

seed = 553

)

SAMPLING FOR MODEL 'anon_model' NOW (CHAIN 1).

Chain 1:

Chain 1: Gradient evaluation took 4e-05 seconds

Chain 1: 1000 transitions using 10 leapfrog steps per transition would take 0.4 seconds.

Chain 1: Adjust your expectations accordingly!

Chain 1:

Chain 1:

Chain 1: Iteration: 1 / 21000 [ 0%] (Warmup)

Chain 1: Iteration: 1001 / 21000 [ 4%] (Sampling)

Chain 1: Iteration: 3100 / 21000 [ 14%] (Sampling)

Chain 1: Iteration: 5200 / 21000 [ 24%] (Sampling)

Chain 1: Iteration: 7300 / 21000 [ 34%] (Sampling)

Chain 1: Iteration: 9400 / 21000 [ 44%] (Sampling)

Chain 1: Iteration: 11500 / 21000 [ 54%] (Sampling)

Chain 1: Iteration: 13600 / 21000 [ 64%] (Sampling)

Chain 1: Iteration: 15700 / 21000 [ 74%] (Sampling)

Chain 1: Iteration: 17800 / 21000 [ 84%] (Sampling)

Chain 1: Iteration: 19900 / 21000 [ 94%] (Sampling)

Chain 1: Iteration: 21000 / 21000 [100%] (Sampling)

Chain 1:

Chain 1: Elapsed Time: 0.407 seconds (Warm-up)

Chain 1: 4.054 seconds (Sampling)

Chain 1: 4.461 seconds (Total)

Chain 1:

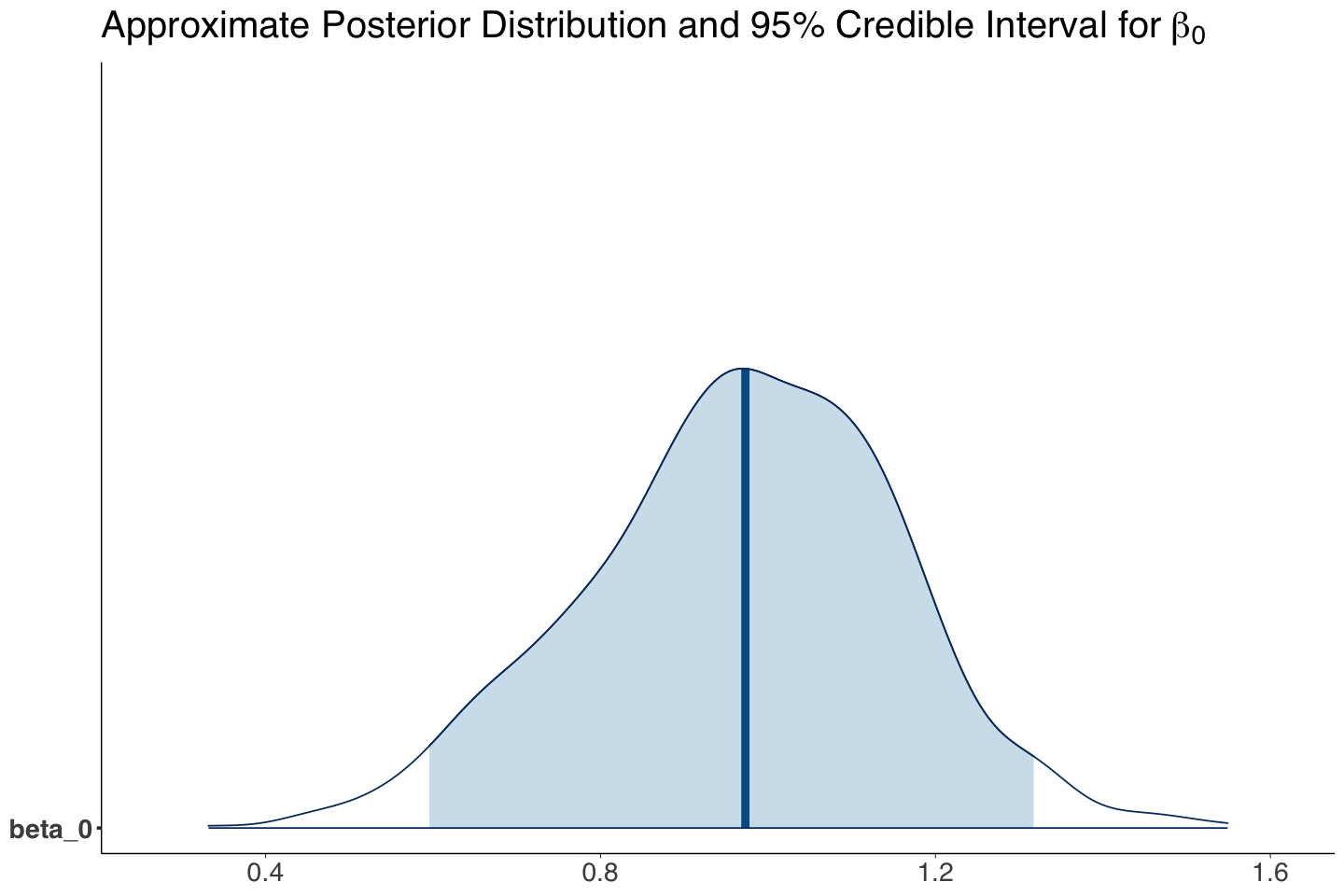

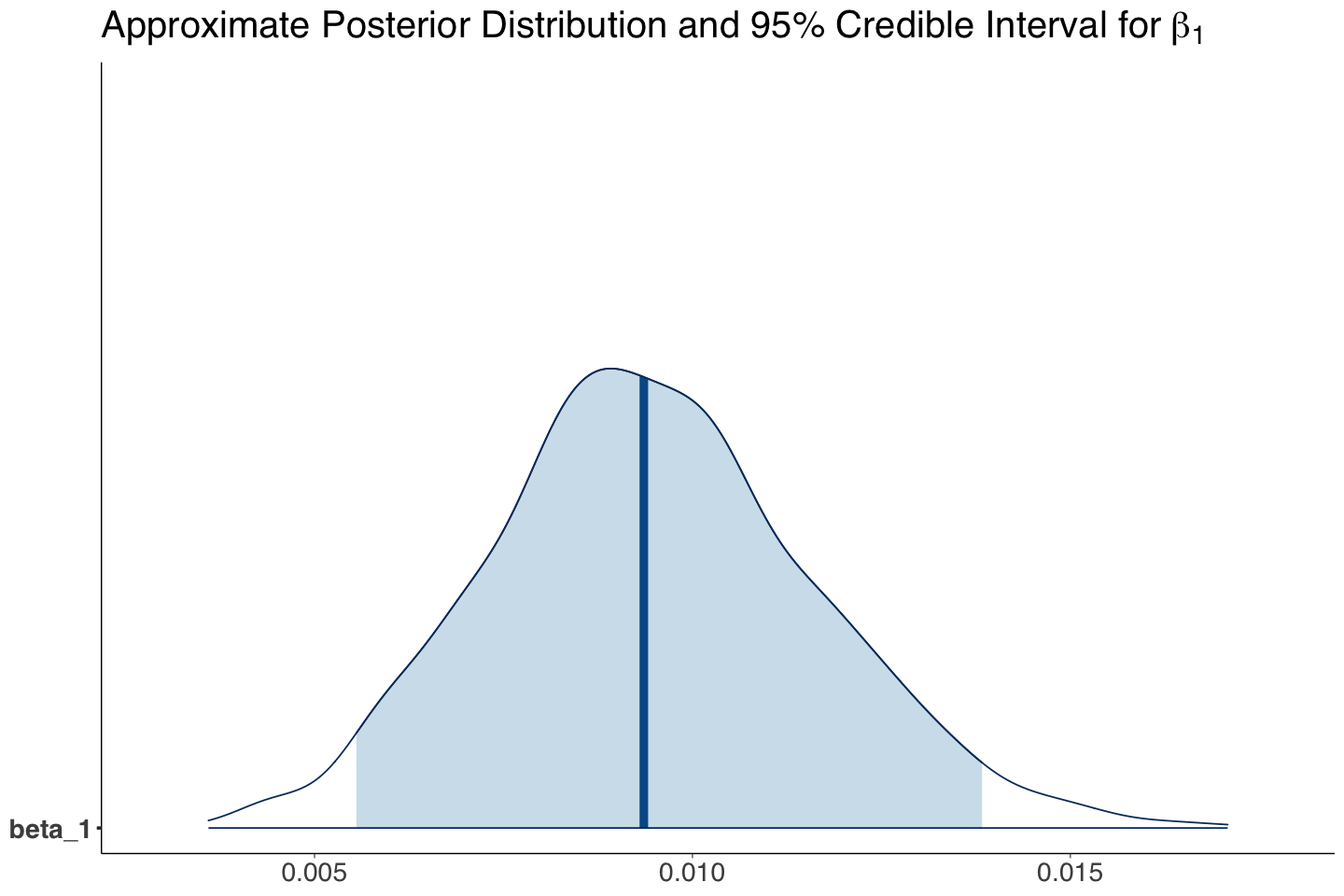

We obtain the posterior summary and compare it versus the tidy() output from the frequentist glm().

posterior_climate_samples <- as.data.frame(summary(posterior_climate)$summary)

posterior_climate_samples <- posterior_climate_samples[, c("mean", "sd", "2.5%", "97.5%")]

posterior_climate_samples <- posterior_climate_samples[1:2,]

posterior_climate_samples |>

mutate(exp_mean = exp(mean), exp_2.5 = exp(`2.5%`), exp_97.5 = exp(`97.5%`)) |>

mutate_if(is.numeric, round, 3)

| mean | sd | 2.5% | 97.5% | exp_mean | exp_2.5 | exp_97.5 | |

|---|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | |

| beta_0 | 0.967 | 0.186 | 0.595 | 1.317 | 2.63 | 1.814 | 3.734 |

| beta_1 | 0.009 | 0.002 | 0.006 | 0.014 | 1.01 | 1.006 | 1.014 |

summary_freq_log_reg

| term | estimate | std.error | statistic | p.value | conf.low | conf.high | exp.estimate | exp.conf.low | exp.conf.high |

|---|---|---|---|---|---|---|---|---|---|

| <chr> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> |

| (Intercept) | 0.965 | 0.184 | 5.248 | 0 | 0.606 | 1.327 | 2.625 | 1.834 | 3.771 |

| income | 0.009 | 0.002 | 4.376 | 0 | 0.005 | 0.014 | 1.009 | 1.005 | 1.014 |

When comparing both approaches, we highlight the following:

The estimates (maximum likelihood-based in

glm()versus the posterior means in the Bayesian approach) are practically equal!The same situation happens regarding variability (column

std.erroringlm()). Recallsdin the Bayesian output refers to the standard deviation from posterior MCMC samples.

There is a big advantage in the Bayesian estimation: we did not need to derive any maximum likelihood steps!

Our Bayesian estimate (i.e., mean of the MCMC posterior samples) for \(\beta_1\) indicates that income is associated with the log of the odds for believing in climate change versus not believing. Since zero is not included in the 95% posterior credible interval, we can conclude this.

The interpretation for the posterior mean of \(\exp(\beta_1)\) is: “for each one thousand USD increase in income, a subject is 1.01 times more likely to believe in climate change than not to”.

beta_0_post_dist <- mcmc_areas(posterior_climate, pars = c("beta_0"), prob = 0.95) +

theme(

plot.title = element_text(size = 24, family = "sans"),

axis.text.x = element_text(size = 17, angle = 0, family = "sans"),

axis.text.y = element_text(size = 17, angle = 0, family = "sans"),

axis.title = element_text(size = 21, family = "sans")

) +

labs(title = expression("Approximate Posterior Distribution and 95% Credible Interval for" ~ beta[0]))

beta_0_post_dist

beta_1_post_dist <- mcmc_areas(posterior_climate, pars = c("beta_1"), prob = 0.95) +

theme(

plot.title = element_text(size = 24, family = "sans"),

axis.text.x = element_text(size = 17, angle = 0, family = "sans"),

axis.text.y = element_text(size = 17, angle = 0, family = "sans"),

axis.title = element_text(size = 21, family = "sans")

) +

labs(title = expression("Approximate Posterior Distribution and 95% Credible Interval for" ~ beta[1]))

beta_1_post_dist

Again, the 1000 posterior samples (pairs containing \(\beta_0\) and \(\beta_1\)) will be use to plot 1000 different sigmoid functions:

The regressor income is set up as a grid from 0 to 500 thousand USD to obtain these 1000 sigmoid functions.

posterior_climate <- as.data.frame(posterior_climate) # posterior_climate as data frame

income <- seq(0, 500, length.out = 500) # Setting up grid for income

beta_0 <- as.numeric(posterior_climate[1, "beta_0"]) # First sample

beta_1 <- as.numeric(posterior_climate[1, "beta_1"]) # First sample

logistic_like <- data.frame(income = income) |> # Computing probabilities with first sample

mutate(values = exp(beta_0 + beta_1 * income) / (1 + exp(beta_0 + beta_1 * income)))

plot_logistic_like_posterior_stanfit <- ggplot(data = logistic_like, na.rm = TRUE) +

geom_line(aes(x = income, y = values), alpha = 0.1, color = "darkred", na.rm = TRUE) +

labs(y = "Probability of Believing Climate is Real", x = "Income (Thousand USD)") +

ggtitle("Posterior Sigmoid Functions") +

theme(

plot.title = element_text(size = 24, face = "bold"),

axis.text = element_text(size = 17),

axis.title = element_text(size = 21)

) # First ggplot layer

for (j in 2:nrow(posterior_climate)) # Loop from the second sample to the last sample in prior_climate

{

beta_0 <- as.numeric(posterior_climate[j, "beta_0"])

beta_1 <- as.numeric(posterior_climate[j, "beta_1"])

logistic_like <- data.frame(income = income) |>

mutate(values = exp(beta_0 + beta_1 * income) / (1 + exp(beta_0 + beta_1 * income)))

plot_logistic_like_posterior_stanfit <- plot_logistic_like_posterior_stanfit +

geom_line(data = logistic_like, aes(x = income, y = values),

alpha = 0.4, color = "darkred", na.rm = TRUE) # Next ggplot layer

}

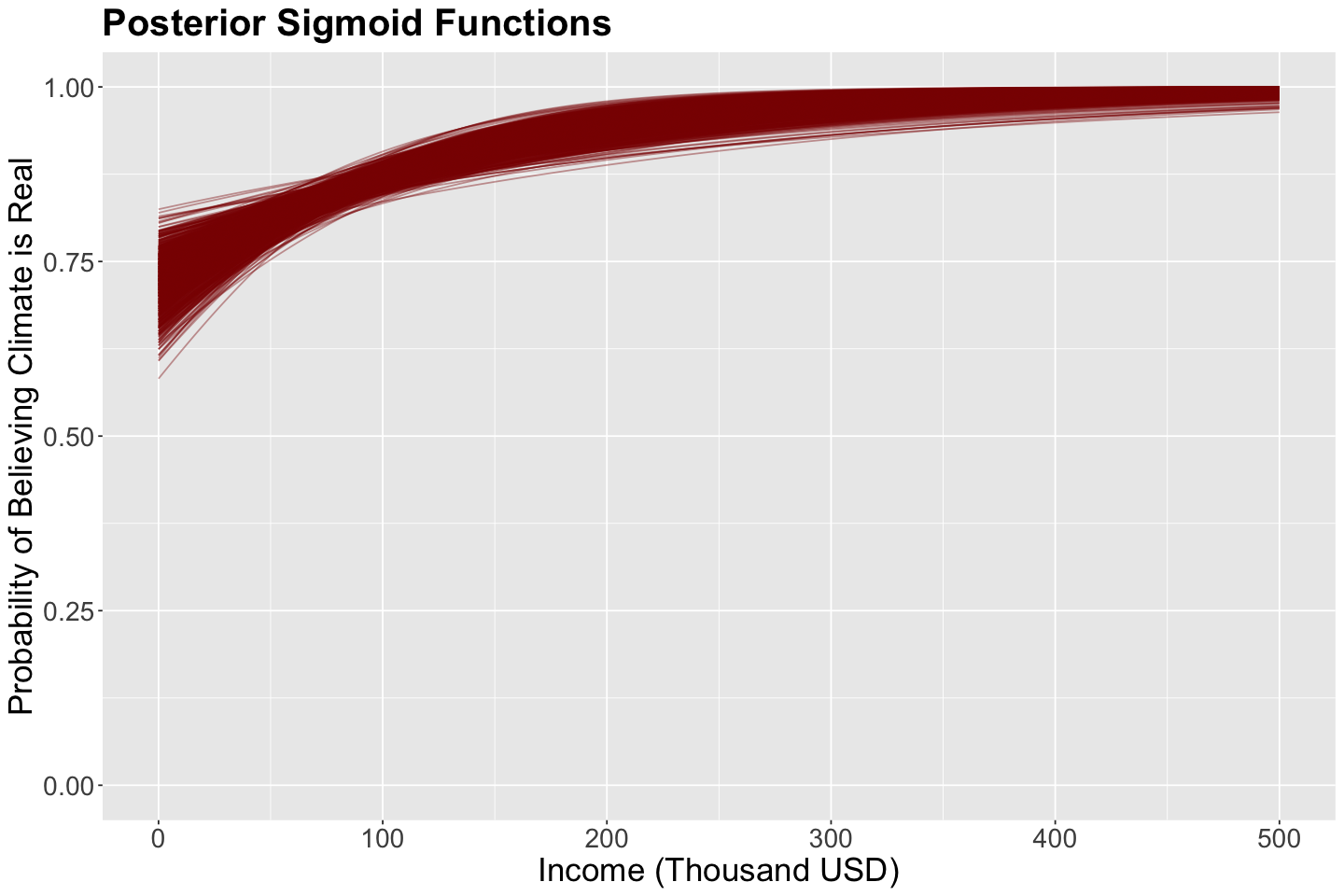

The plot below shows these 1000 sigmoid functions. This is a posterior distribution over curves (since a curve is defined by \(\beta_0\) and \(\beta_1\)). Hence, these red sigmoid curves are samples from this distribution.

plot_logistic_like_posterior_stanfit + ylim(0, 1)

Now, we have a clear pattern in this posterior distribution! This is the likelihood (i.e., your data) in conjunction with the prior distribution via the Bayes’ rule.

plot_grid(plot_logistic_like_prior_stanfit, plot_logistic_like_posterior_stanfit)

4.5. Distributions of Predicted Probabilities#

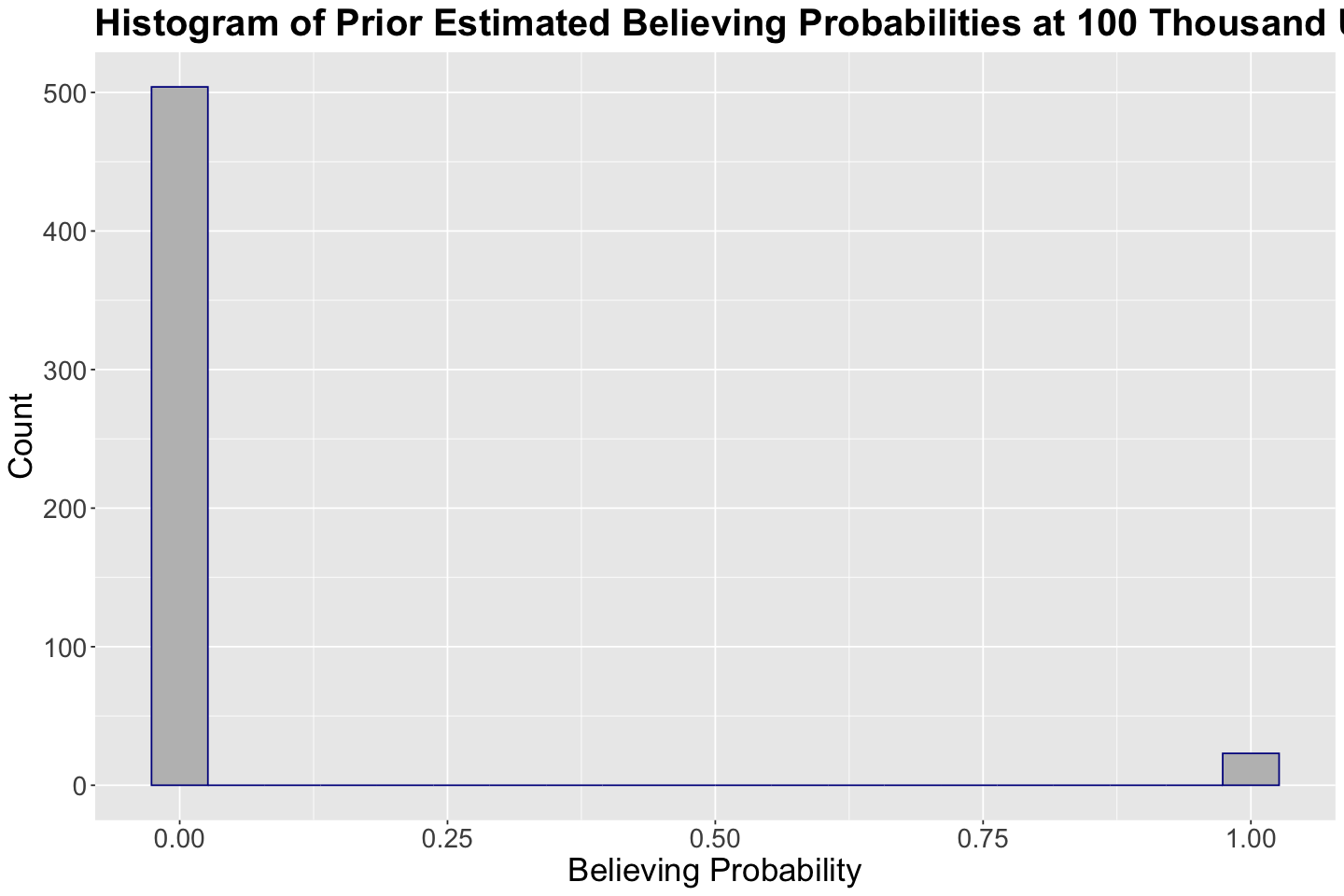

Suppose you want to obtain the prior distribution of predicted probabilities of success (i.e., a subject believing in climate change) with an income of 100 thousand USD. We will use our 1000 prior samples in prior_climate for \(\beta_0\) and \(\beta_1\) to do so.

Note you will find NaNs in some rows since the predicted probabilities are so small that we encounter numerical errors.

prior_climate <- prior_climate |>

mutate(probability_believing = exp(beta_0 + beta_1 * 100) / (1 + exp(beta_0 + beta_1 * 100)))

head(prior_climate)

| beta_0 | beta_1 | lp__ | probability_believing | |

|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | |

| 1 | -1.496540 | 130.56652 | -0.8524928 | NaN |

| 2 | 24.444430 | 155.43653 | -1.2379023 | NaN |

| 3 | 59.631513 | -21.02121 | -0.1998904 | 0 |

| 4 | -4.196843 | 69.27654 | -0.2408426 | NaN |

| 5 | 40.825609 | 28.84540 | -0.1249394 | NaN |

| 6 | -48.995753 | 84.73686 | -0.4790460 | NaN |

We were not able to compute the 1000 prior probabilities. Nonetheless, the ones we could calculate are zero or close to zero. Therefore, this is not an informative predictive distribution for an income of 100 thousand USD.

hist_100_prior <- prior_climate |>

ggplot() +

geom_histogram(aes(probability_believing), fill = "grey", color = "darkblue", bins = 20, na.rm = TRUE) +

theme(

plot.title = element_text(size = 24, face = "bold"),

axis.text = element_text(size = 17),

axis.title = element_text(size = 21)

) +

ggtitle("Histogram of Prior Estimated Believing Probabilities at 100 Thousand USD") +

labs(x = "Believing Probability", y = "Count")

hist_100_prior

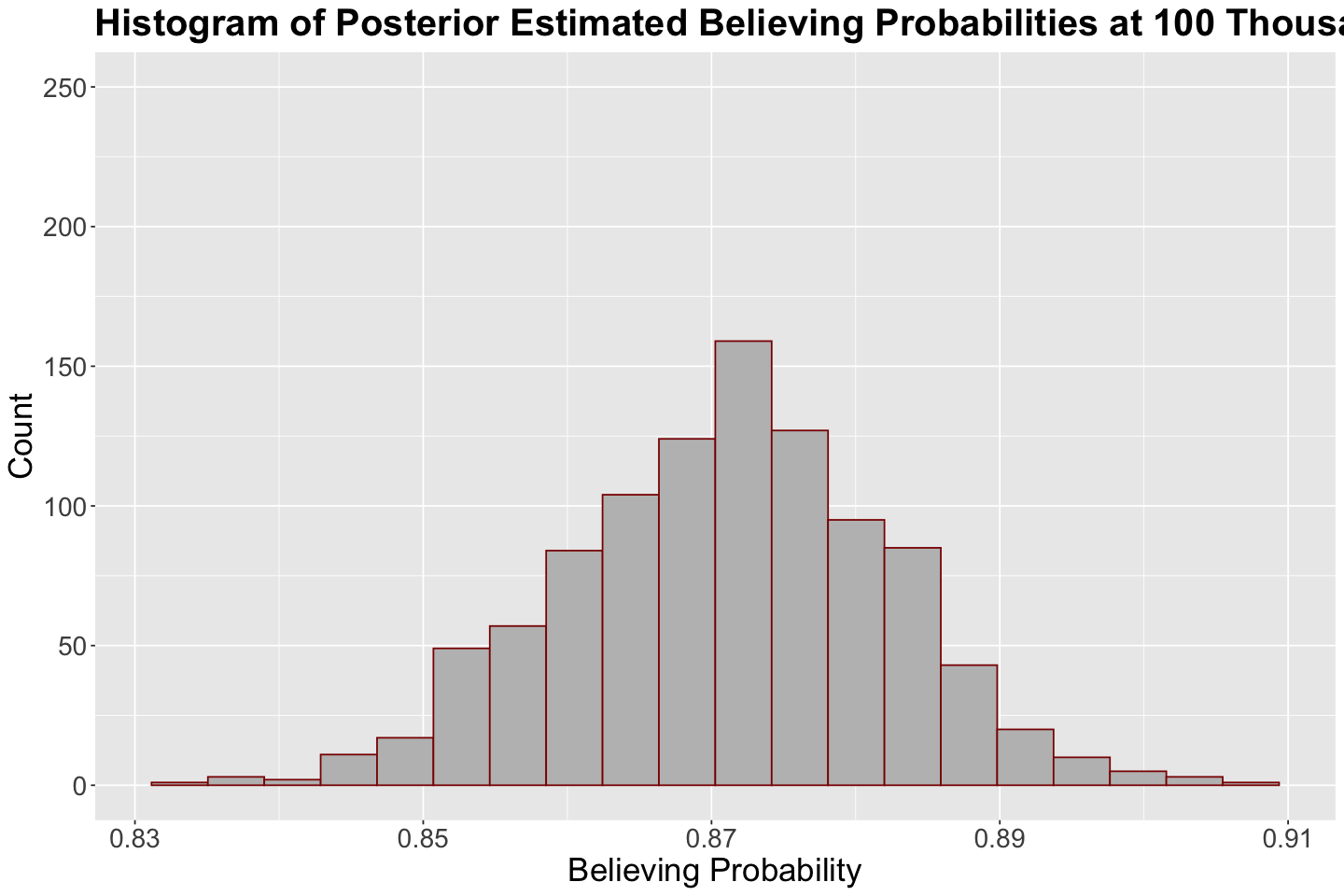

Now, let us follow the same process with posterior_climate.

posterior_climate <- posterior_climate |>

mutate(probability_believing = exp(beta_0 + beta_1 * 100) / (1 + exp(beta_0 + beta_1 * 100)))

head(posterior_climate)

round(mean(posterior_climate$probability_believing), 2) # Mean predicted probability

| beta_0 | beta_1 | lp__ | probability_believing | |

|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | |

| 1 | 0.9704702 | 0.007264117 | -413.4656 | 0.8451271 |

| 2 | 0.7640832 | 0.012281058 | -412.2110 | 0.8799745 |

| 3 | 0.8504562 | 0.010322106 | -411.5658 | 0.8679171 |

| 4 | 1.0570489 | 0.009500551 | -411.9428 | 0.8815409 |

| 5 | 0.7329129 | 0.011229681 | -412.2951 | 0.8648161 |

| 6 | 1.0641366 | 0.009201498 | -411.7768 | 0.8791374 |

The predictive posterior distribution for the probability of success is more reasonable! We have a mean prediction of 0.87. The distribution is relatively symmetric. With an income of 100 thousand USD, the posterior predicted probability leans more towards believing in climate change.

hist_100_posterior <- posterior_climate |>

ggplot() +

geom_histogram(aes(probability_believing), fill = "grey", color = "darkred", bins = 20) +

theme(

plot.title = element_text(size = 24, face = "bold"),

axis.text = element_text(size = 17),

axis.title = element_text(size = 21)

) +

ggtitle("Histogram of Posterior Estimated Believing Probabilities at 100 Thousand USD") +

labs(x = "Believing Probability", y = "Count")

hist_100_posterior + ylim(0, 250)

5. Wrapping Up#

We extended Bayesian regression to a GLM approach while keeping one of the core components: the link function.

The inferential conclusions are done as in Bayesian Normal regression.

We can also build posterior predictive distributions in a Binary Logistic regression framework.

This Bayesian GLM approach can be applied to other models of this class with the proper arrangements (e.g., count regression, multinomial logistic regression, etc.).