Fundamentals of the Multivariate Normal Distribution

This appendix will start with some basics on plotting multidimensional probability density functions (PDFs). Then, we will recheck the concepts of independence and dependence from DSCI 551 along with its visualization. Finally, we will wrap up the appendix with the bivariate and multivariate Normal distributions and some exercises (with their corresponding solutions at the end of the appendix).

1 Drawing Multidimensional Functions

Drawing a \(d\)-dimensional PDF requires \(d + 1\) dimensions, so we usually draw \(1\)-dimensional functions and occasionally draw \(2\)-dimensional functions.

A common way to draw \(2\)-dimensional functions (not just PDFs!) is to use contour plots. To understand countour plots, you can think of the output dimension as coming out of the page. Here are some examples of how to draw \(2\)-dimensional functions: in Python and in R.

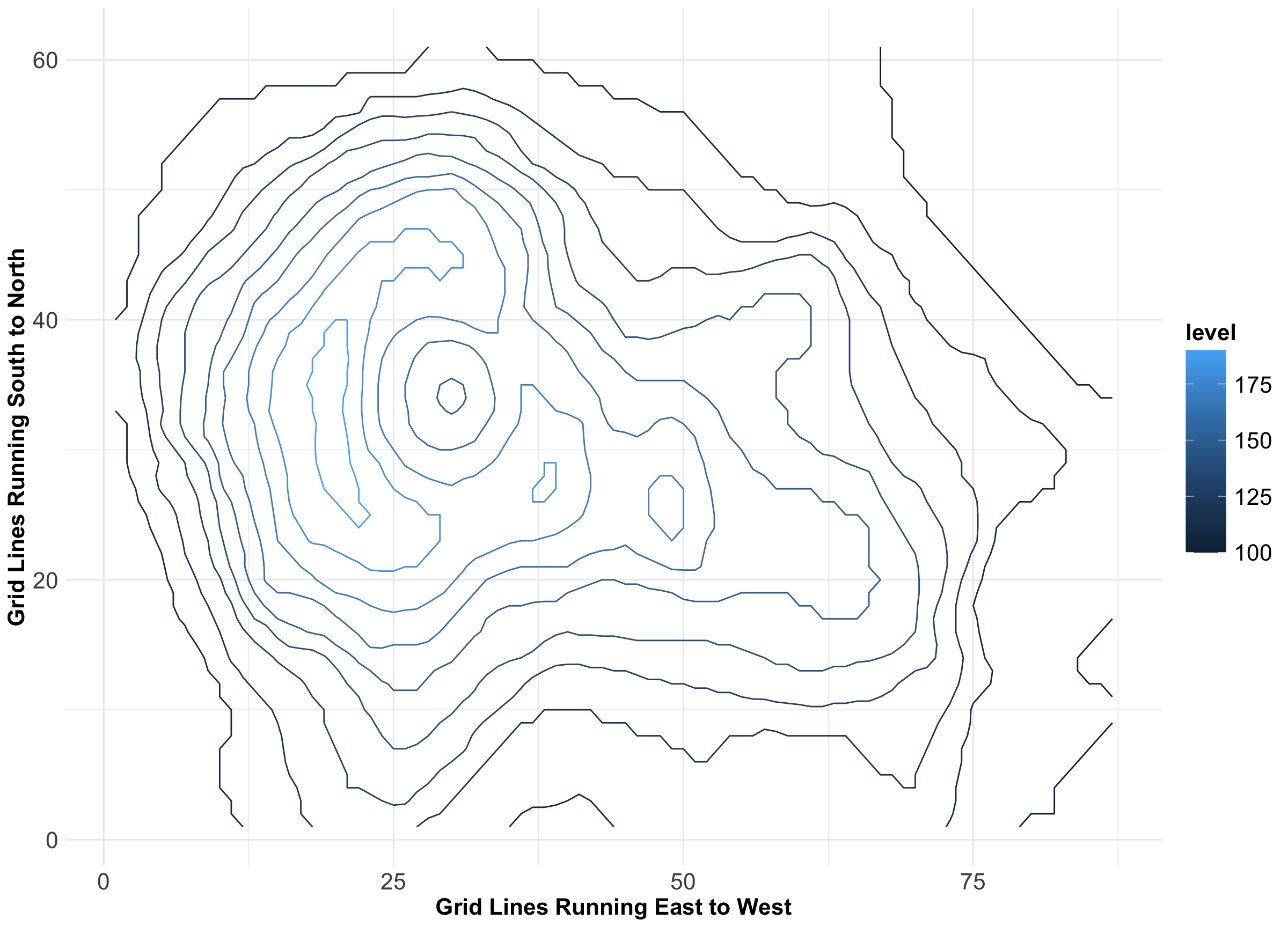

As an additional example, we provide a contour plot rendering of the elevation of Auckland’s Maunga Whau Volcano. According to the dataset documentation in Figure 1, the \(x\)-axis indicates grid lines running east to west, whereas the \(y\)-axis indicates grid lines running south to north. Note that this plot has a legend indicating the volcano’s elevation in metres as a colour scale for the corresponding contours.

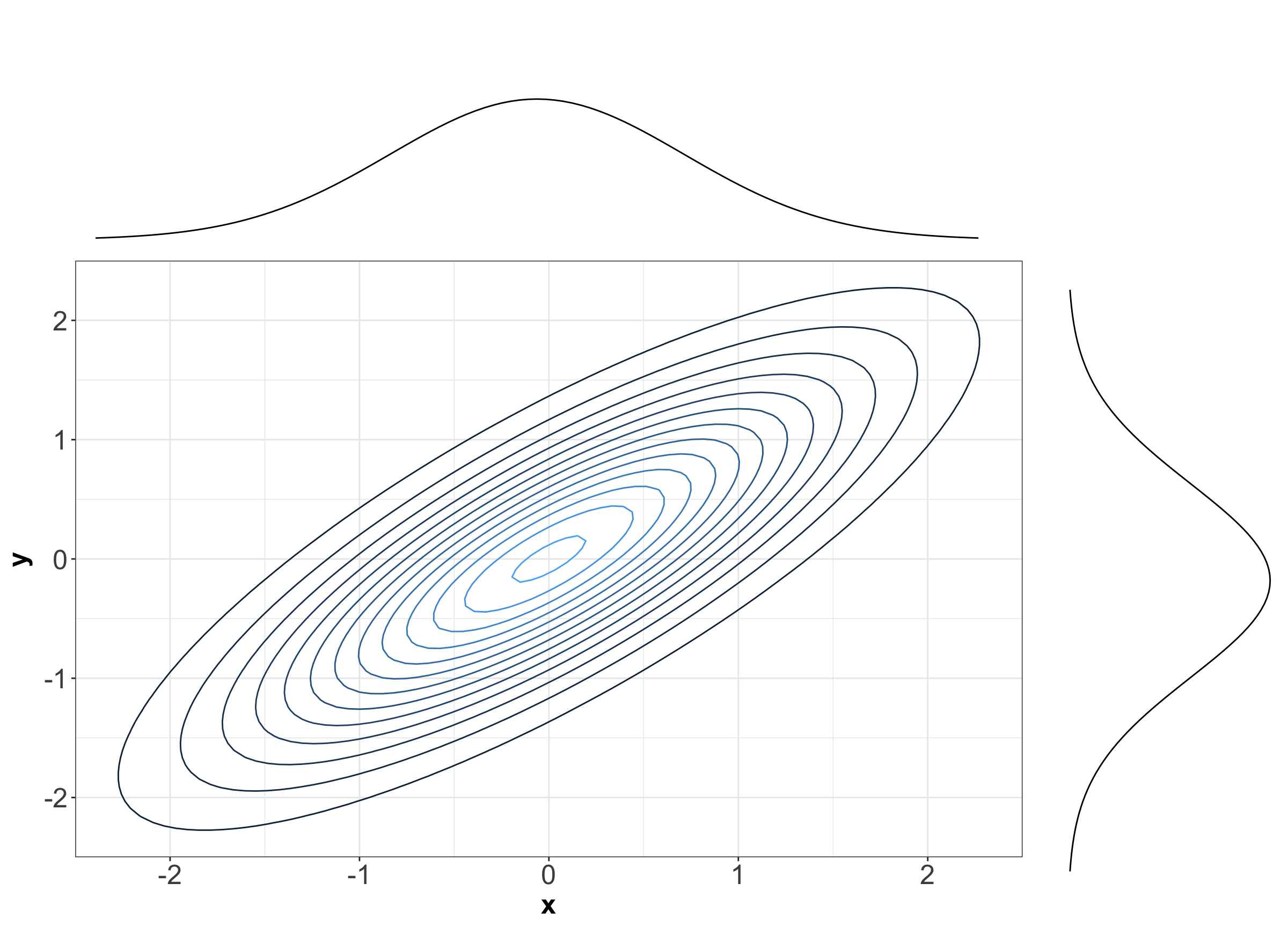

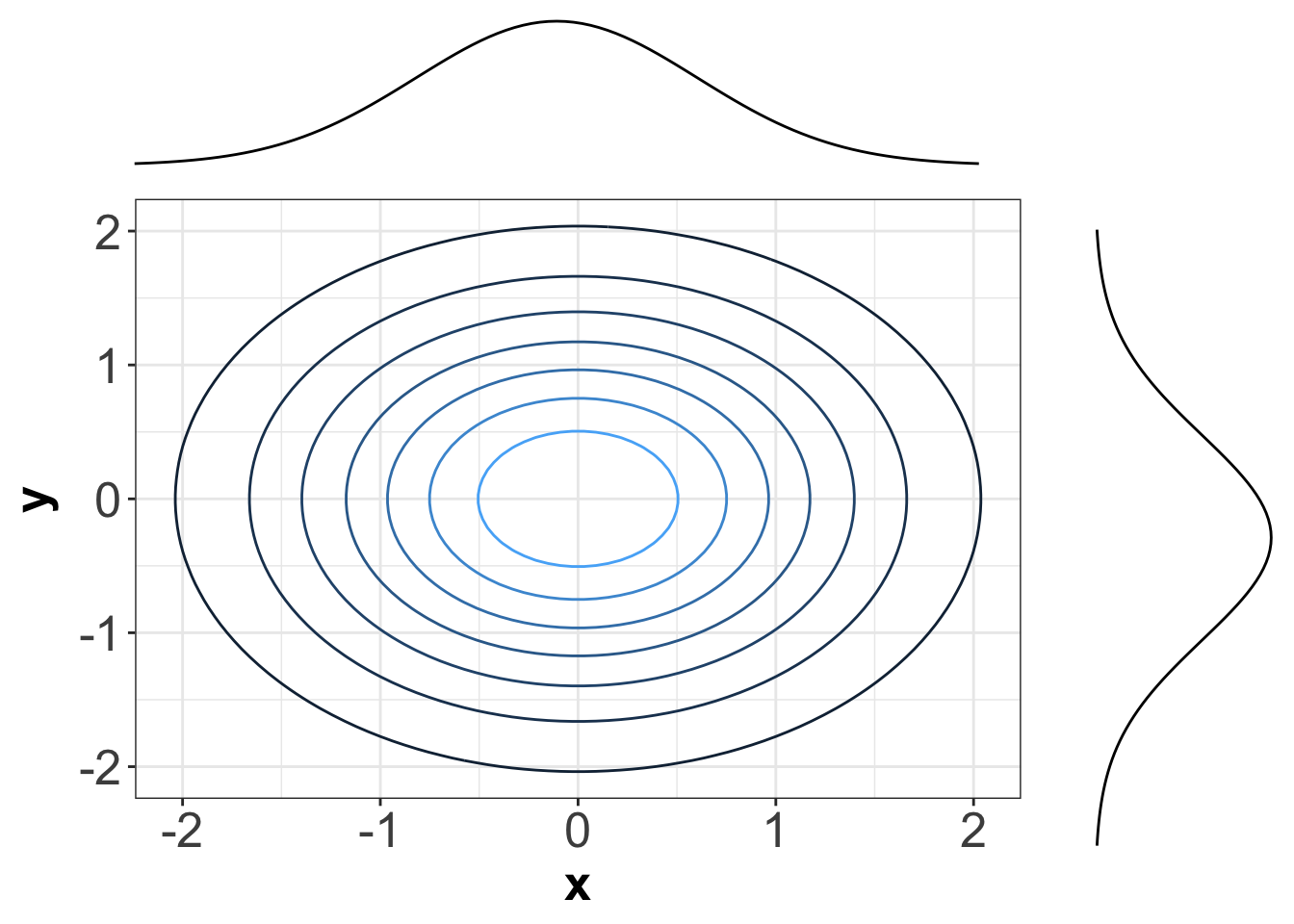

Let us start with theoretical contour plots in multivariate continuous distributions. When it comes to bivariate PDFs, it is informative to plot the marginal densities on each axis. Figure 2 is an example where marginals are Normal or Gaussian, and the joint distribution is also a bivariate Normal or Gaussian (we will see what this means later on in this appendix!).

Figure 2 shows the contours corresponding to the density of a bivariate Normal distribution (imagine the PDF is on a third \(z\)-axis coming out from the screen). The numeric levels as a legend corresponding to the multivariate PDF were omitted to leave room for the corresponding marginal Normal PDFs of random variable \(X\) on top and random variable \(Y\) on the right-hand side.

In Figure 3, we can also check the three-dimensional plot corresponding to the contour plot in Figure 2 (we include the legend corresponding to the probability density on the \(z\)-axis):

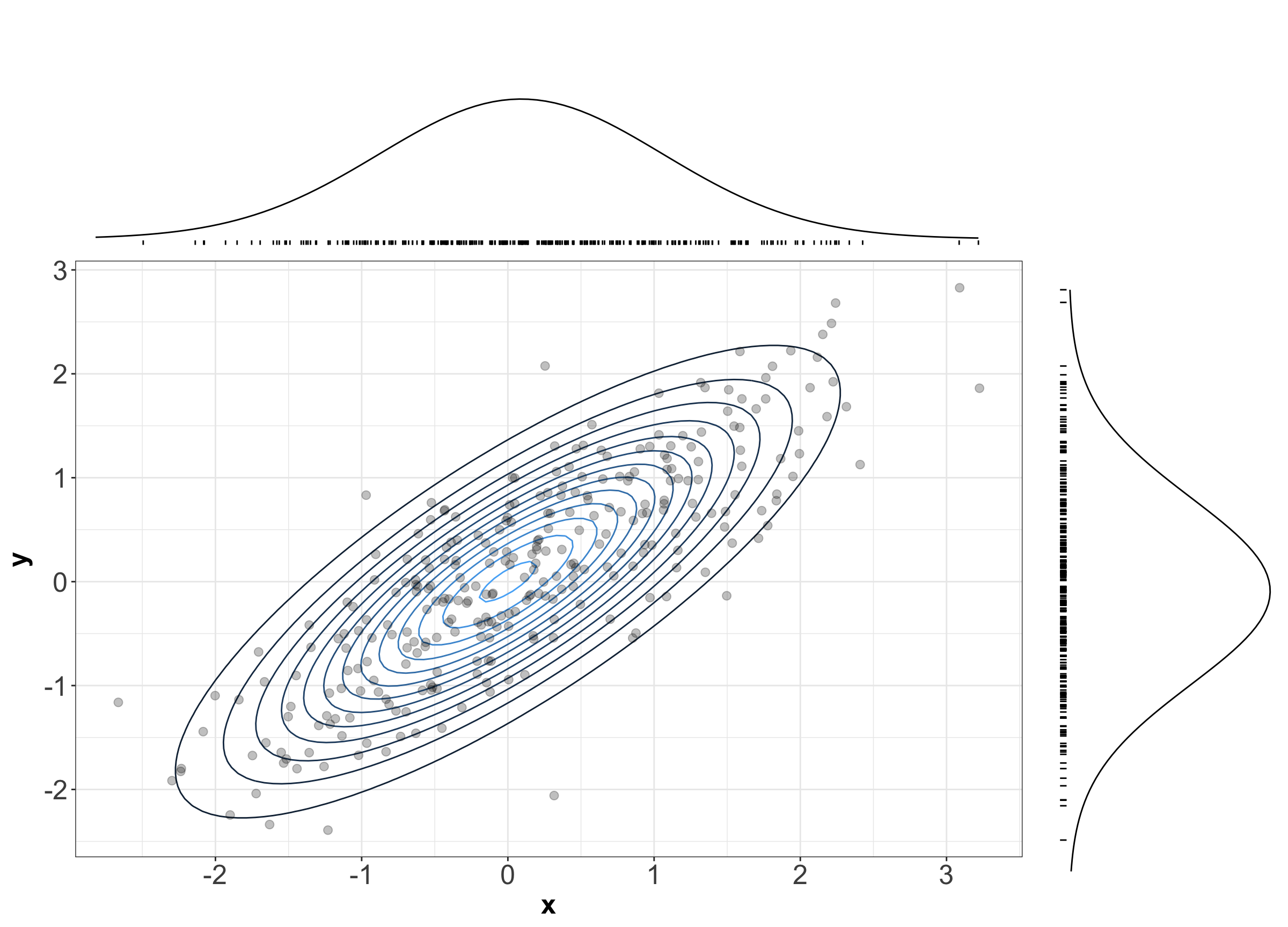

Recall the PDF tells us how “densely packed” data coming from this distribution will be. Figure 4 show the same contour plot from Figure 2, but with a sample of size \(n = 300\) data points plotted overtop. The individual \(x\) and \(y\) coordinates are also plotted with their corresponding densities. Notice that points are more densely packed near the middle, where the density function is biggest.

2 Independence

Let us revisit the concept of probabilistic independence but applied to multivariate continuous distributions.

2.1 Definition in the Continuous Case

Recall that the independence of random variables \(X\) and \(Y\) means that knowledge about one variable tells us nothing about the other.

Definition of independence in probability distributions between two random variables

Let \(X\) and \(Y\) be two independent random variables. Using their corresponding marginals, we can obtain their corresponding joint distributions as follows:

- \(X\) and \(Y\) are discrete. Let \(P(X = x, Y = y)\) be the joint probability mass function (PMF) with \(P(X = x)\) and \(P(Y = y)\) as their marginals. Then, we define the joint PMF as:

\[P(X = x, Y = y) = P(X = x) \cdot P(Y = y).\]

- \(X\) and \(Y\) are continuous. Let \(f_{X,Y}(x,y)\) be the joint PDF with \(f_X(x)\) and \(f_Y(y)\) as their marginals. Then, we define the joint PDF as:

\[f_{X,Y}(x,y) = f_X(x) \cdot f_Y(y).\]

Important

The term denoting a discrete joint PMF \(P(X = x, Y = y)\) is equivalent to the intersection of events \(P(X = x \cap Y = y)\).

In the discrete case, this means that a joint probability distribution (when depicted as a table) has each row/column as a multiple of the others because (by definition of independence):

\[P(X = x \cap Y = y) = P(X = x) \cdot P(Y = y).\]

Or, equivalently,

\[P(Y = y \mid X = x) = \frac{P(X = x \cap Y = y)}{P(X = x)} = \frac{P(X = x) \cdot P(Y = y)}{P(X = x)} = P(Y = y).\]

In the continuous case, probabilities become densities. A definition of independence becomes

\[ f_{X,Y}(x, y) = f_X(x) \cdot f_Y(y), \tag{1}\]

where \(f_{X,Y}(x, y)\) is the joint PDF of the continuous random variables \(X\) and \(Y\), \(f_X(x)\) is the marginal PDF of \(X\), and \(f_Y(y)\) is the marginal PDF of \(Y\). Or, equivalently

\[ f_{Y \mid X}(y) = \frac{f_{X,Y}(x, y)}{f_X(x)}= \frac{f_X(x) \cdot f_Y(y)}{f_X(x)} = f_Y(y). \tag{2}\]

Important

Each of these two above definitions has an intuitive meaning. The first definition,

\[ f_{X,Y}(x, y) = f_X(x) \cdot f_Y(y) \]

in Equation 1, means that, when slicing the joint density at various points along the \(x\)-axis (and also for the \(y\)-axis), the resulting one-dimensional function will be the same, except for some multiplication factor. For example,

\[ f_{X,Y}(1, y) = f_X(1) \cdot f_Y(y) \]

and

\[ f_{X,Y}(2, y) = f_X(2) \cdot f_Y(y). \]

So \(f_{X,Y}(1, y)\) and \(f_{X,Y}(2,y)\) are actually the same function, just scaled by different factors. Note that \(f_{X,Y}(1,y)\) is NOT a proper PDF.

The second definition,

\[ f_{Y \mid X}(y) = f_Y(y) \]

in Equation 2, is probably more intuitive. As in the discrete case, it means that knowing \(X\) does not tell us anything about \(Y\). The same could be said about the reverse. To see why definition in Equation 1 is equivalent to the definition in Equation 2, consider the below formula, which holds regardless of whether we have independence:

\[ f_{X,Y}(x, y) = f_{Y \mid X}(y) \ f_X(x). \]

Setting \(f_{Y \mid X}(\cdot)\) equal to \(f_Y(\cdot)\) results in the original definition from Equation 1.

2.2 Independence Visualized

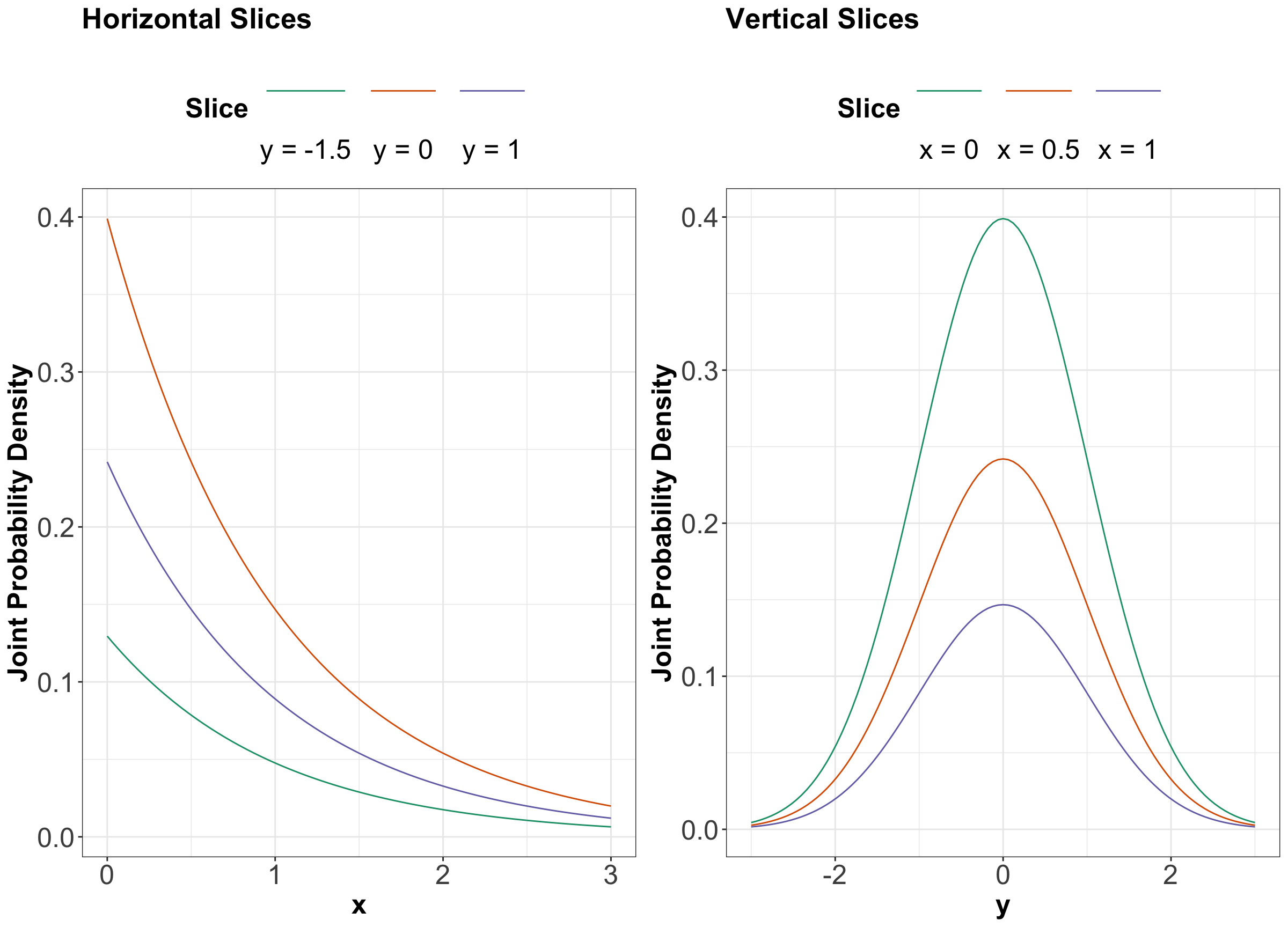

Let us start with theoretical contour plots in multivariate continuous distributions. When it comes to bivariate PDFs, it is informative to plot the marginal densities on each axis. In general, just by looking at a contour plot of a bivariate density function, it is hard to tell whether this distribution is of two independent random variables. But we can tell by looking at “slices” of the distribution.

Here is an example of two independent random variables where

\[X \sim \text{Exponential}(\lambda = 1),\]

and

\[Y \sim \mathcal{N}\left(\mu = 0, \sigma^2 = 1\right).\]

Mathematically, their joint PDF is expressed as:

\[ \begin{align*} f_{X,Y} \left( x, y \right) &= f_X \left( x \mid \lambda = 1 \right) \times f_Y \left( y \mid \mu = 0, \sigma^2 = 1 \right) \\ &= \left[ \lambda \exp(-\lambda x) \right] \times \left\{ \frac{1}{\sqrt{2\pi \sigma^2}} \exp \left[ -\frac{(y - \mu)^2}{2\sigma^2} \right] \right\} \\ &= \exp(-x) \times \left[ \frac{1}{\sqrt{2\pi}} \exp \left( -\frac{y^2}{2} \right) \right]. \end{align*} \]

Their corresponding joint PDF is shown in Figure 5.

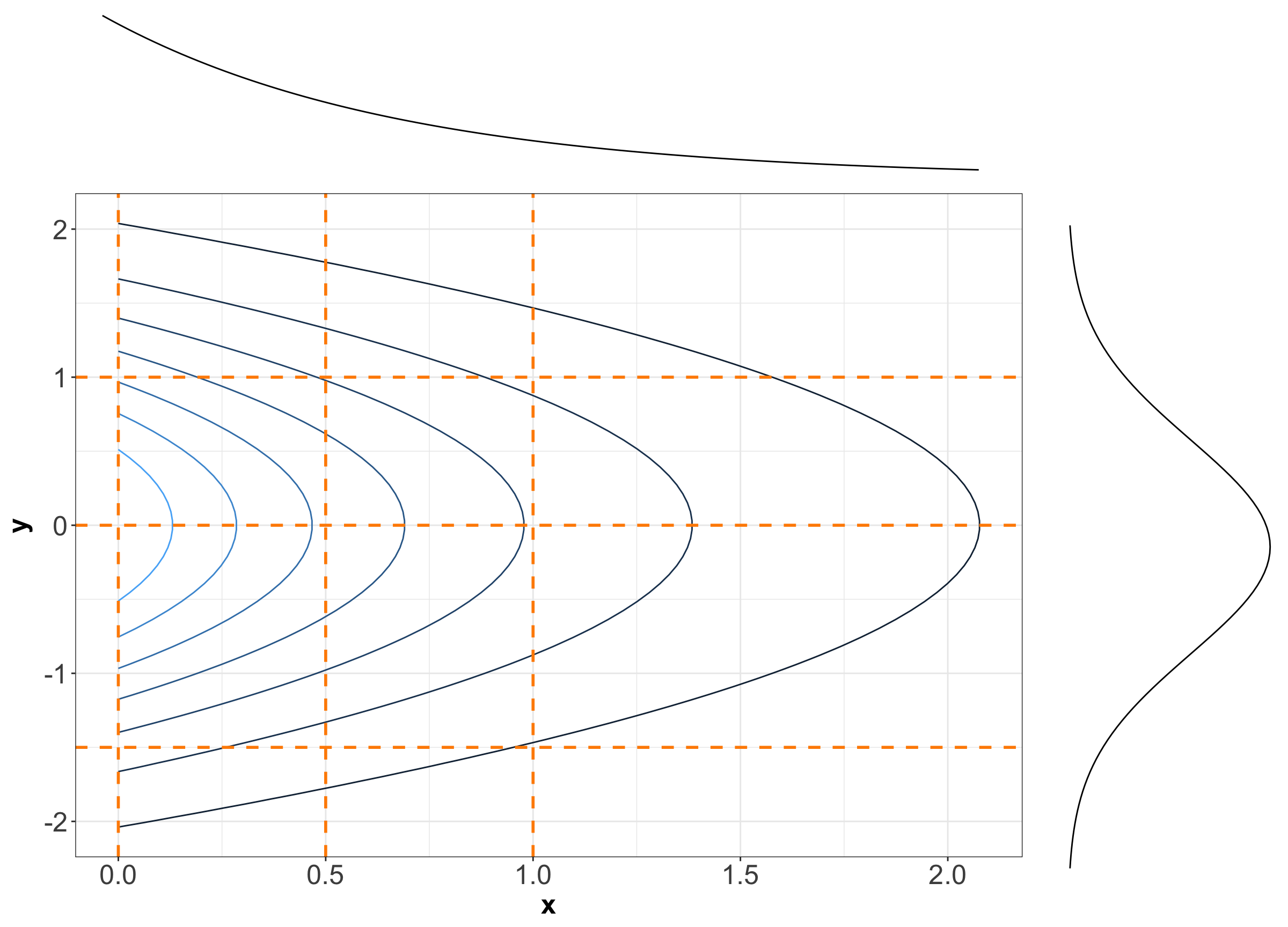

Now, the three-dimensional plot from Figure 5 also has a contour version, as shown in Figure 6. We will slice this contour plot along the dashed orange lines.

In Figure 7, you can find the slices in each case denoted by the previous dashed orange lines. We can see that these slices resemble the form of Exponential distributions for \(x\) and Normal distributions for \(y\).

Again, in Figure 7, it is not that each vertical (or horizontal) slice is the same, but they are all the same when the slice is normalized. In other words, every slice has the same shape.

What do we get when we normalize these slices so that the curves have an area of 1 underneath? By definition, we get the conditional distributions given the slice value. And, these conditional distributions will be the exact same (one for each axis \(x\) and \(y\)) since the sliced densities only differ by a multiple anyway. What is more, this common distribution is just the marginal.

Mathematically, what we are saying is

\[f_{Y \mid X}(y) = \frac{f_{X,Y}(x,y)}{f_X(x)} = \frac{f_{X}(x) \cdot f_{Y}(y)}{f_X(x)} = f_Y(y).\]

And we have the same for \(X \mid Y\). Again, we are back to the definition of independence!

Now, here is an example where we have two independent Standard Normal distributions \(X\) and \(Y\) whose marginals are the following:

\[ \begin{gather*} X \sim \mathcal{N}(\mu_X = 0, \sigma^2_X = 1) \\ Y \sim \mathcal{N}(\mu_Y = 0, \sigma^2_Y = 1). \end{gather*} \]

Important

In general, not just in the case of joint distributions, we say that a Normal random variable is Standard Normal when its mean equals \(0\) and its variance equals 1.

Their joint PDF is:

\[ \begin{align*} f_{X,Y} \left( x, y \right) &= f_X \left( x \mid \mu_X = 0, \sigma_X^2 = 1 \right) \times f_Y \left( y \mid \mu_Y = 0, \sigma_Y^2 = 1 \right) \\ &= \left\{ \frac{1}{\sqrt{2\pi \sigma_X^2}} \exp \left[ -\frac{(x - \mu_X)^2}{2\sigma_X^2} \right] \right\} \times \\ & \qquad \left\{ \frac{1}{\sqrt{2\pi \sigma_Y^2}} \exp \left[ -\frac{(y - \mu_Y)^2}{2\sigma_Y^2} \right] \right\} \\ &= \left[ \frac{1}{\sqrt{2\pi}} \exp \left( -\frac{x^2}{2} \right) \right] \times \left[ \frac{1}{\sqrt{2\pi}} \exp \left( -\frac{y^2}{2} \right) \right]. \end{align*} \tag{3}\]

Equation 3 is the joint PDF of a bivariate Normal or Gaussian.

Important

Figure 8 shows the contour plot of the bivariate Normal distribution (from Equation 3) composed of two independent Standard Normal distributions \(X\) and \(Y\). Note the contours are perfectly centred in the middle, which graphically implies independence.

If \(X\) and \(Y\) were not independent, then these contours would appear in a diagonal pattern.

Its corresponding three-dimensional plot is shown in Figure 9.

3 Dependence

Two variables can be dependent in a multitude of ways, but usually, there is an overall direction of dependence:

- Positively related random variables tend to increase together. That is, larger values of \(X\) are associated with larger values of \(Y\).

- Negatively related random variables have an inverse relationship. That is, larger values of \(X\) are associated with smaller values of \(Y\).

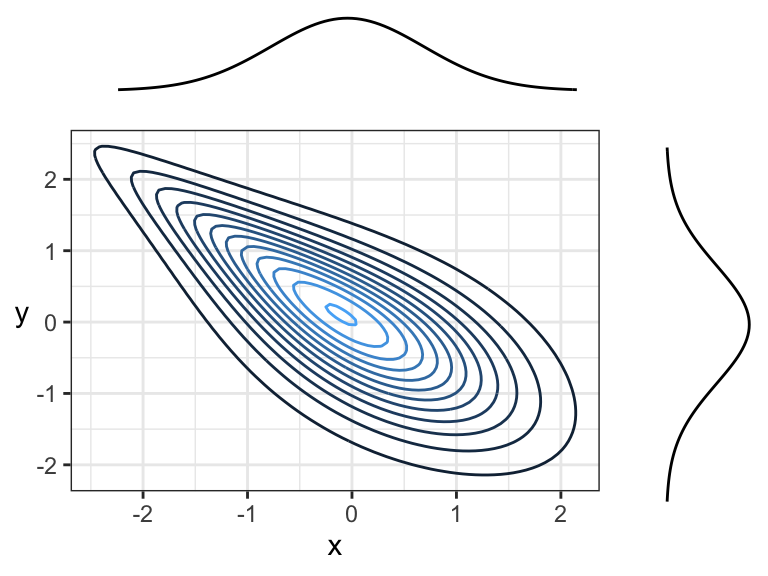

Figure 10 shows two positively correlated continuous variables, because there is an overall tendency of the contour lines to point up and to the right (or down and to the left).

Figure 11 shows two negatively correlated continuous variables, because there is an overall tendency for the contour lines to point down and to the right (or up and to the left):

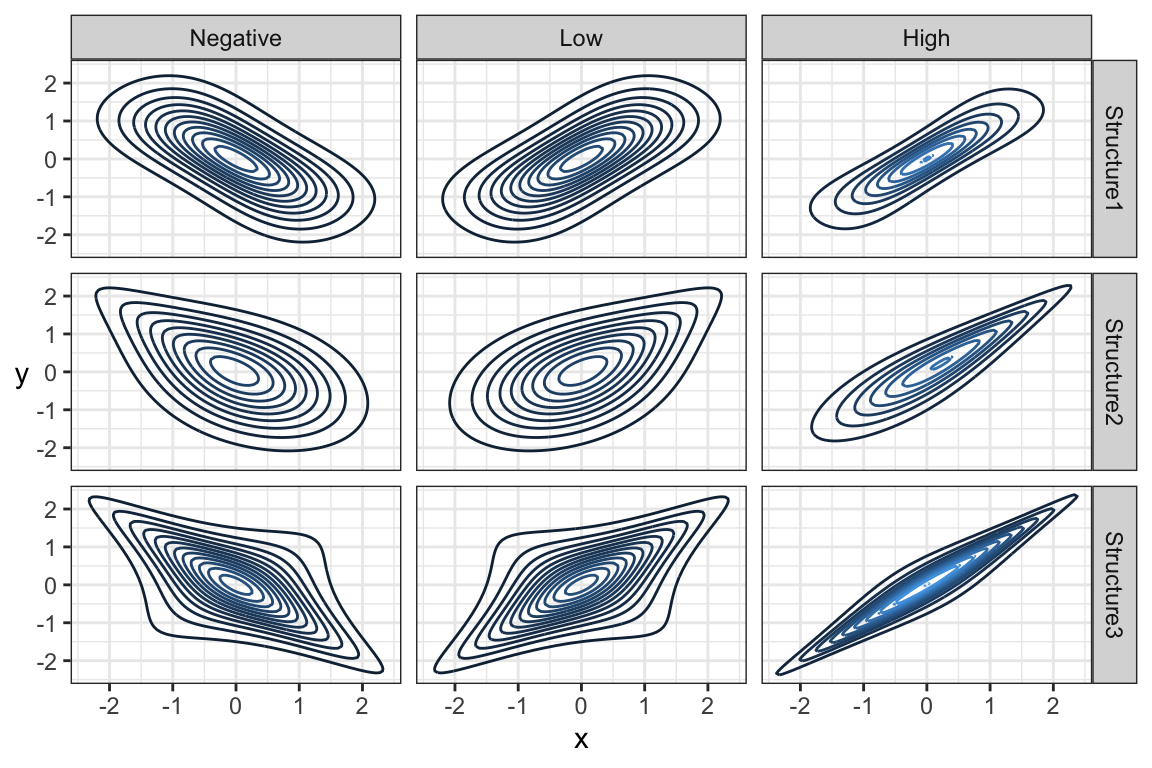

Note that the marginal distributions have nothing to do with the dependence between random variables. Here are some examples of joint distributions that all have the same marginals, namely

\[\mathcal{N}(\mu = 0, \sigma^2 = 1),\]

but different dependence structures and strengths of dependence. Specifically, we have

\[X \sim \mathcal{N}(\mu_x = 0, \sigma_x^2 = 1)\]

and

\[Y \sim \mathcal{N}(\mu_y = 0, \sigma_y^2 = 1),\]

but \((X,Y)\) is not jointly Gaussian for these 9 densities (see Figure 12).

This echoes the idea that if you are given the marginals of

\[X \sim \mathcal{N}(\mu_x = 0, \sigma_x^2 = 1)\]

and

\[Y \sim \mathcal{N}(\mu_y = 0, \sigma_y^2 = 1),\]

there are (infinitely) many joint distributions that have these marginals. In short, just because you know the marginals, you cannot assume you know the joint distribution unless the variables are independent. Hence, when \(X\) and \(Y\) are independent, their joint density is given by:

\[f_{X,Y}(x, y) = f_{X}(x) \cdot f_{Y}(y).\]

4 Multivariate Normal or Gaussian Family

We have already seen the Normal or Gaussian family of univariate distributions. There is also a multivariate family of Gaussian distributions.

Important

Members of this family need to have all Gaussian marginals, and their dependence has to be Gaussian. Gaussian dependence is obtained as a consequence of requiring that any linear combination of Gaussian random variables is also Gaussian.

4.1 Parameters in a Multivariate Normal or Gaussian Distribution

To characterize the bivariate Gaussian family (i.e., \(d = 2\) involved random variables), we need the following parameters:

- Means for both \(X\) and \(Y\) denoted as \(-\infty < \mu_X < \infty\) and \(-\infty < \mu_Y < \infty\), respectively.

- Variances for both \(X\) and \(Y\) denoted as \(\sigma^2_X > 0\) and \(\sigma^2_Y > 0\), respectively.

- The covariance between \(X\) and \(Y\), sometimes denoted \(\sigma_{XY}\) or, equivalently, the Pearson correlation denoted \(-1 \leq \rho_{XY} \leq 1\).

That is five parameters altogether; and only one of them, Pearson correlation or covariance, is needed to specify the dependence part in a bivariate Gaussian family. Now, let us define the PDF of the bivariate Gaussian or Normal Distribution in scalar notation(i.e., without vectors or matrices).

Definition of a bivariate Normal or Gaussian distribution

Let \(X\) and \(Y\) be two random variables with means \(-\infty < \mu_X < \infty\) and \(-\infty < \mu_Y < \infty\), variances \(\sigma^2_X > 0\) and \(\sigma^2_Y > 0\), a Pearson correlation coefficient \(-1 \leq \rho_{XY} \leq 1\). Then, $ X$ and \(Y\) have a bivariate Normal or Gaussian distribution if the joint PDF is:

\[ \begin{align*} f_{XY}\left(x, y \mid \mu_X, \mu_Y, \sigma^2_X, \sigma^2_Y, \rho_{XY}\right) &= \frac{1}{2 \pi \sigma_X \sigma_Y \sqrt{1 - \rho_{XY}^2}} \times \\ & \qquad \exp \Bigg\{ - \frac{1}{2 \left( 1 - \rho_{XY}^2 \right)} \Big[ \left( \frac{x - \mu_X}{\sigma_X} \right)^2 + \\ & \qquad \quad \left( \frac{y - \mu_Y}{\sigma_Y} \right)^2 - \\ & \qquad \qquad 2 \rho_{XY} \frac{\left( x - \mu_X \right) \left( y - \mu_Y \right)}{\sigma_X \sigma_Y} \Big] \Bigg\}. \end{align*} \tag{4}\]

Using the parameters of a bivariate Gaussian distribution, we can construct two objects that are useful for computations: a mean vector \(\boldsymbol{\mu}\) and a covariance matrix \(\boldsymbol{\Sigma}\), where

\[ \boldsymbol{\mu}=\begin{pmatrix} \mu_X \\ \mu_Y \end{pmatrix} \]

and

\[ \boldsymbol{\Sigma} = \begin{pmatrix} \sigma_X^2 & \sigma_{XY} \\ \sigma_{XY} & \sigma_Y^2 \end{pmatrix}. \tag{5}\]

Important

Notice that \(\sigma_{XY}\) is repeated in the upper-right and lower-left corner of \(\boldsymbol{\Sigma}\). We call this kind of matrix a symmetric matrix. It happens that symmetric matrices simplify many of the computations we will do down the road.

Note that the covariance matrix is always defined as in in Equation 5. Even if we are given the correlation \(\rho_{XY}\), instead of the covariance \(\sigma_{XY}\), we would then need to calculate the covariance as

\[\sigma_{XY} = \rho_{XY} \sigma_X \sigma_Y\]

before constructing the covariance matrix. However, there is another matrix that is sometimes useful, called the correlation matrix \(\mathbf{P}\). Firstly, let us recall the formula of the Pearson correlation between \(X\) and \(Y\):

\[\rho_{XY} = \frac{\operatorname{Cov}(X, Y)}{\sqrt{\operatorname{Var}(X)\operatorname{Var}(Y)}} = \frac{\sigma_{XY}}{\sqrt{\sigma_X^2 \sigma_Y^2}}.\]

Now, what happens to the Pearson correlation of a random variable with itself (i.e., \(\rho_{XX}\) and \(\rho_{YY}\))? It turns out that:

\[ \begin{gather*} \rho_{XX} = \frac{\operatorname{Cov}(X, X)}{\sqrt{\operatorname{Var}(X)\operatorname{Var}(X)}} = \frac{\text{Var}(X)}{\sqrt{\sigma^2_X \sigma^2_X}} = \frac{\sigma^2_X}{\sigma^2_X} = 1 \\ \rho_{YY} = \frac{\operatorname{Cov}(Y, Y)}{\sqrt{\operatorname{Var}(Y)\operatorname{Var}(Y)}} = \frac{\text{Var}(Y)}{\sqrt{\sigma^2_Y \sigma^2_Y}} = \frac{\sigma^2_Y}{\sigma^2_Y} = 1. \end{gather*} \]

Thus, correlation matrix \(\mathbf{P}\) is defined as:

\[ \begin{align*} \mathbf{P} &= \begin{pmatrix} \frac{\sigma^2_X}{\sigma^2_X} & \frac{\sigma_{XY}}{\sqrt{\sigma_X^2 \sigma_Y^2}} \\ \frac{\sigma_{XY}}{\sqrt{\sigma_X^2 \sigma_Y^2}} & \frac{\sigma^2_Y}{\sigma^2_Y} \end{pmatrix} \\ &= \begin{pmatrix} \rho_{XX} & \rho_{XY} \\ \rho_{XY} & \rho_{YY} \end{pmatrix} \\ &= \begin{pmatrix} 1 & \rho_{XY} \\ \rho_{XY} & 1 \end{pmatrix}. \end{align*} \]

This linear algebra format of the parameters also makes it easier to generalize to more than two variables (i.e., \(d > 2\)).

In general, the multivariate Gaussian distribution of \(d\) variables has some generic \(d\)-dimensional mean vector and a \(d \times d\) covariance matrix, where the upper-right and lower-right triangles of the covariance matrix are the same. This means that to fully specify this \(d\)-dimensional distribution, we need:

- the means and variances of all \(d\) random variables, and

- the covariance or correlations between each pair of random variables, i.e., \(d \choose 2\) pairs of them.

It turns out any square matrix is a valid covariance matrix, so long as it is symmetric and positive semi-definite. This ensures that each variance is not negative and that \(-1 \leq \rho_{ij} \leq 1\) (i.e., each element of the correlation matrix \(\mathbf{P}\)). Thus, it ensures

\[ | \text{Cov}(X,Y) | \leq \sqrt{\text{Var}(X) \text{Var}(Y)}. \]

Now, let us check an example with \(d = 3\) whose random variables are \(X\), \(Y\), and \(Z\). The covariance matrix is given by:

\[ \boldsymbol{\Sigma} = \begin{pmatrix} \sigma_X^2 & \sigma_{XY} & \sigma_{XZ} \\ \sigma_{XY} & \sigma_Y^2 & \sigma_{YZ}\\ \sigma_{XZ} & \sigma_{YZ} & \sigma_Z^2 \end{pmatrix}, \]

where the elements of the main diagonal correspond to the marginal variances \(\sigma_X^2\), \(\sigma_Y^2\), and \(\sigma_Z^2\). On the other hand, the off-diagonal elements correspond to the covariances \(\sigma_{XY}\), \(\sigma_{XZ}\), and \(\sigma_{YZ}\). The correlation matrix with \(d = 3\) will be:

\[ \mathbf{P} = \begin{pmatrix} 1 & \rho_{XY} & \rho_{XZ} \\ \rho_{XY} & 1 & \rho_{YZ}\\ \rho_{XZ} & \rho_{YZ} & 1 \end{pmatrix}. \]

Overall with \(d = 3\), there are 9 parameters needed to characterize the Gaussian family:

- 3 for the marginal means \(\mu_X\), \(\mu_Y\), and \(\mu_Z\).

- 3 for the marginal variances \(\sigma_X^2\), \(\sigma_Y^2\), and \(\sigma_Z^2\).

- 3 for all the possible pairwise covariances \(\sigma_{XY}\), \(\sigma_{XZ}\), and \(\sigma_{YZ}\).

Important

Note we do not include the Pearson correlations \(\rho_{XY}\), \(\rho_{XZ}\), and \(\rho_{YZ}\) in this set of 9 parameters, given they are already in function of the corresponding marginal variances and pairwise covariances.

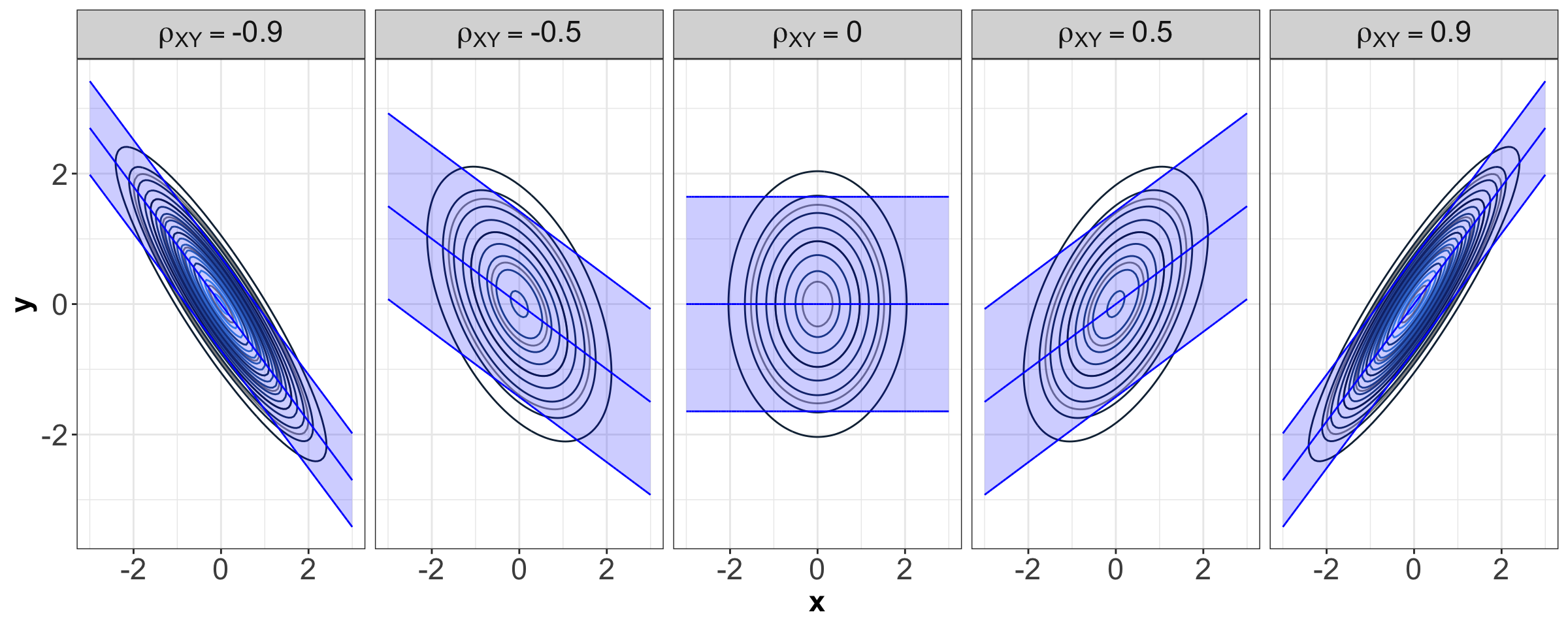

4.2 Visualizing Bivariate Normal or Gaussian Densities

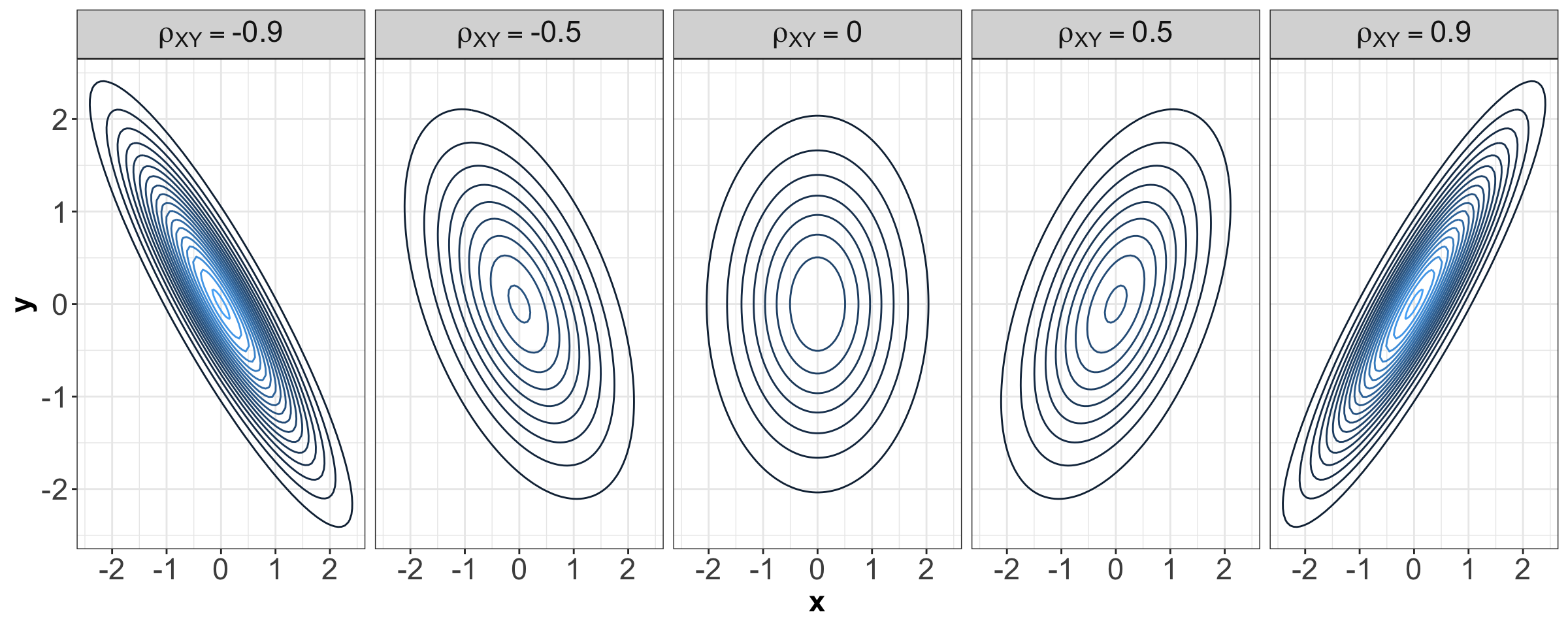

The joint density of a bivariate Normal or Gaussian distribution has a characteristic elliptical shape. Figure 13 shows some examples with \(\mathcal{N}(0, 1)\) marginals for \(X\) and \(Y\) and different Pearson correlations indicated in the grey title bars.

Important

Note that, when \(\rho_{xy} = 0\), the contours are perfectly centred in the middle. Hence, we might wonder what we meant by contours perfectly centred in the middle in the above bivariate Normal case composed of two independent Standard Normal distributions, so let us explore the five panels from Figure 13.

An essential component of a bivariate Normal distribution is the Pearson correlation coefficient, which measures linear dependency between \(X\) and \(Y\). For our marginal Standard Normal random variables \(X\) and \(Y\), let us define their Pearson correlation coefficient as \(\rho_{XY}\). Overall, the five panels indicate the following:

- When \(X\) and \(Y\) are independent, by definition of independence, their \(\rho_{XY} = 0\) (as in the above panel in the middle). Therefore, their contours are perfectly centred in the middle.

- On the other hand, when \(X\) and \(Y\) are not independent, their \(\rho_{XY} \neq 0\) (as in the other four panels above). Note their contours have a diagonal pattern.

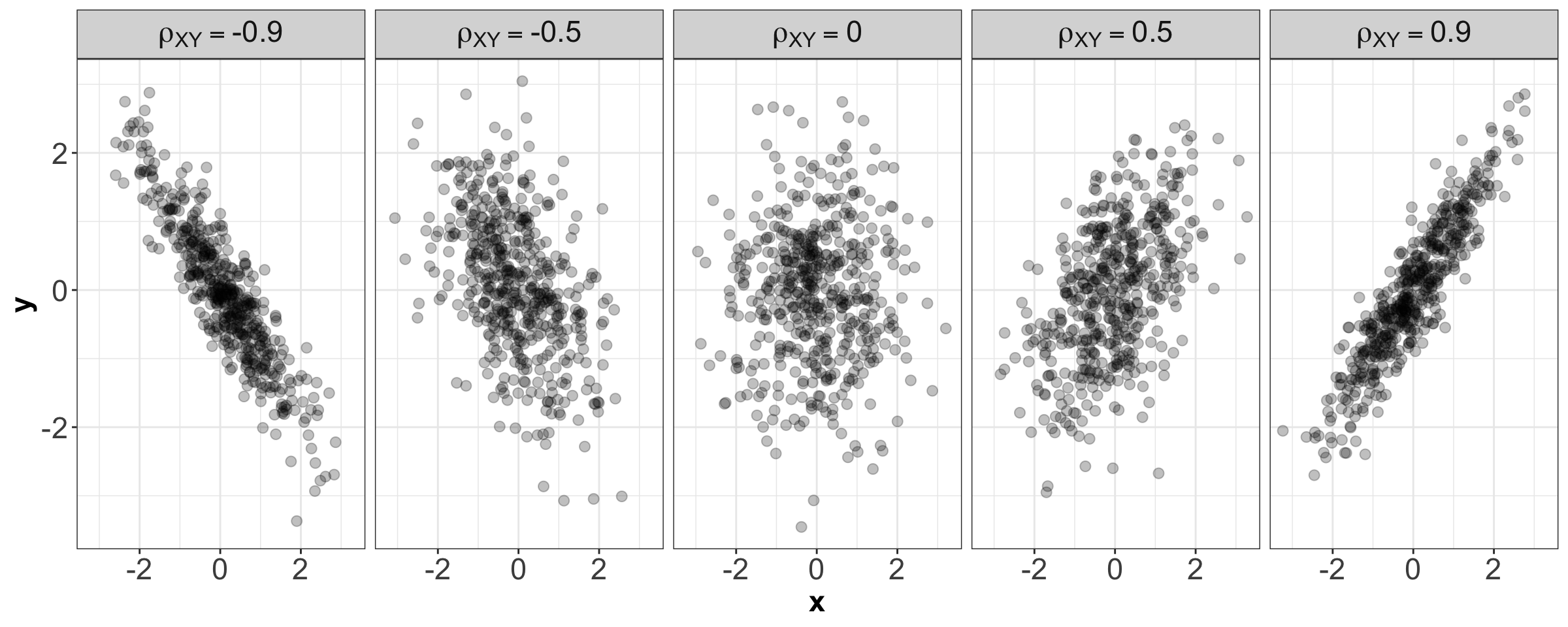

Additionally, in Figure 14, you can find five samples of size \(n = 500\) each of data coming from the distributions in Figure 13 under different values of \(\rho_{XY}\).

Important

Let us discuss the case of an uncorrelated bivariate Gaussian (i.e., \(\rho_{XY} = 0\)). This case implies that \(X\) and \(Y\) are independent. But, remember in general, uncorrelated often does not imply independence.

Note

The above statement is proved if we work around via the PDF from Equation 4 with \(\rho_{XY} = 0\):

\[ \begin{align*} f_{XY}\left(x, y \mid \mu_X, \mu_Y, \sigma^2_X, \sigma^2_Y, \rho_{XY} = 0 \right) &= \frac{1}{2 \pi \sigma_X \sigma_Y \sqrt{1 - \rho_{XY}^2}} \times \\ & \qquad \exp \Bigg\{ - \frac{1}{2 \left( 1 - \rho_{XY}^2 \right)} \Big[ \left( \frac{x - \mu_X}{\sigma_X} \right)^2 + \\ & \qquad \quad \left( \frac{y - \mu_Y}{\sigma_Y} \right)^2 - 2 \rho_{XY} \frac{\left( x - \mu_X \right) \left( y - \mu_Y \right)}{\sigma_X \sigma_Y} \Big] \Bigg\} \\ &= \frac{1}{2 \pi \sigma_X \sigma_Y} \times \qquad \qquad \qquad \quad \text{ we let }\rho_{XY} = 0 \\ & \qquad \quad \exp \left\{ - \frac{1}{2} \left[ \left( \frac{x - \mu_X}{\sigma_X} \right)^2 + \left( \frac{y - \mu_Y}{\sigma_Y} \right)^2 \right] \right\} \\ &= \frac{1}{\sqrt{2 \pi \sigma_X^2} \sqrt{ 2 \pi \sigma_Y^2}} \times \qquad \qquad \text{rearranging terms}\\ & \qquad \exp \left[-\frac{1}{2} \left( \frac{x - \mu_X}{\sigma_X} \right)^2 \right] \times \\ & \qquad \quad \exp \left[-\frac{1}{2} \left( \frac{y - \mu_Y}{\sigma_Y} \right)^2 \right] \\ &= \underbrace{\frac{1}{\sqrt{2 \pi \sigma_X^2}} \exp \left[-\frac{1}{2} \left( \frac{x - \mu_X}{\sigma_X} \right)^2 \right]}_{f_X(x \mid \mu_X, \sigma_X^2)} \times \\ & \qquad \underbrace{\frac{1}{\sqrt{2 \pi \sigma_Y^2}} \exp \left[-\frac{1}{2} \left( \frac{y - \mu_Y}{\sigma_Y} \right)^2 \right]}_{f_Y(y \mid \mu_Y, \sigma_Y^2)}. \end{align*} \]

The above last line corresponds to the mathematical definition of independence provided in Equation 1. Moreover, \(f_X(x \mid \mu_X, \sigma_X^2)\) and \(f_Y(y \mid \mu_Y, \sigma_Y^2)\) correspond to the marginal distributions

\[X \sim \mathcal{N}(\mu_X, \sigma_X^2)\]

and

\[Y \sim \mathcal{N}(\mu_Y, \sigma_Y^2),\]

respectively.

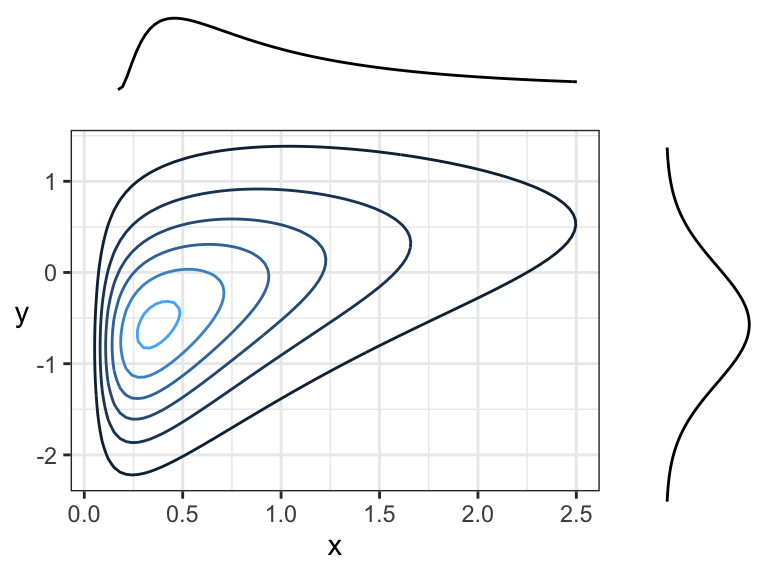

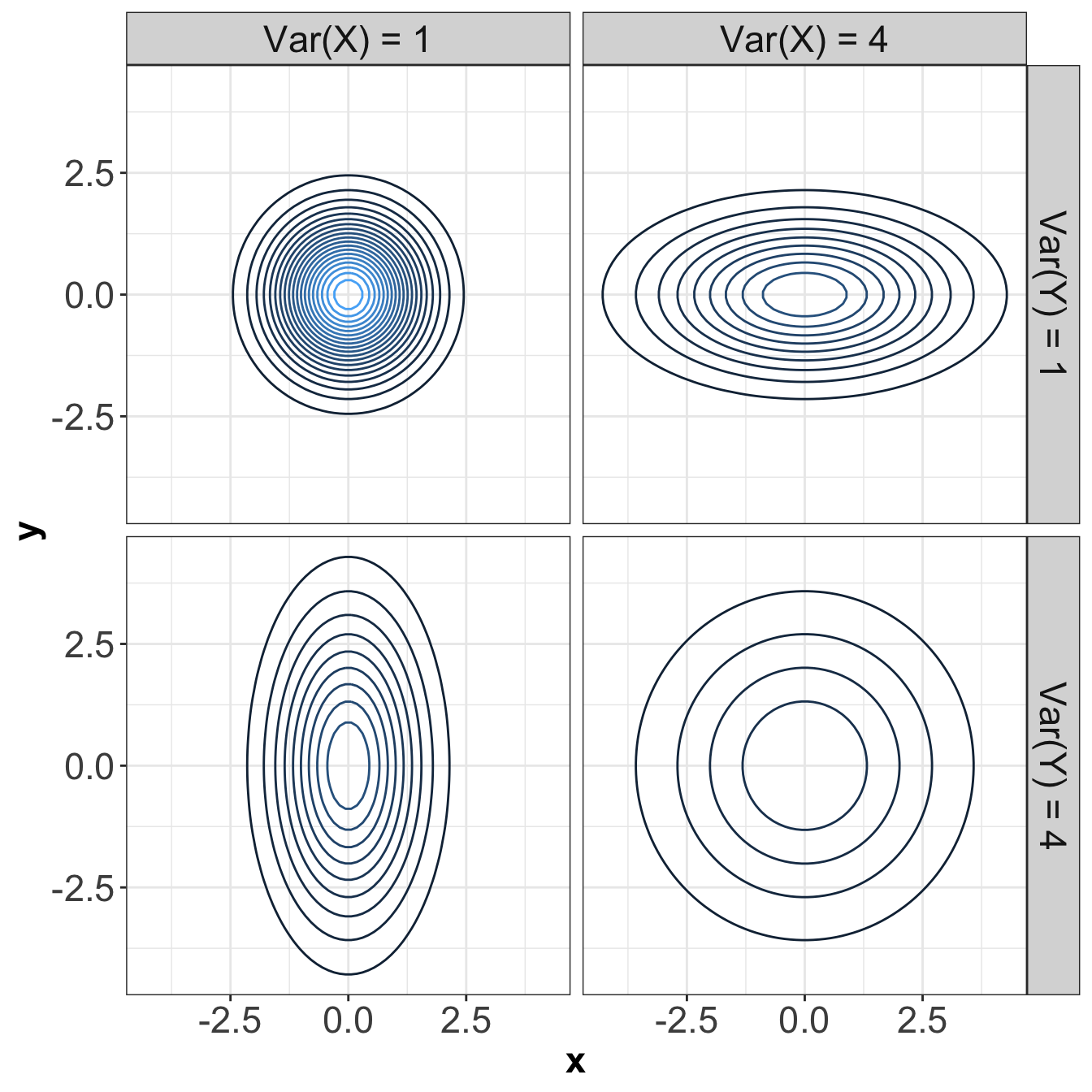

Let us take a look at uncorrelated densities in Figure 15, but with different variances, and means of \(0\).

In Figure 15, notice that elliptical contours stretched either vertically or horizontally still have no dependence! The stretch needs to be on some diagonal for there to be dependence – that is, pointing in some direction other than along the \(x\)-axis or \(y\)-axis. Circular contours are both independent, and each marginal has the same variance.

4.3 Properties

A bivariate Normal or Gaussian distribution has the following properties:

- Marginal distributions are Gaussian. The marginal distribution of a subset of variables can be obtained by just taking the relevant subset of means, and the relevant subset of the covariance matrix.

- Linear combinations are Gaussian. This is actually by definition. If \((X, Y)\) have a bivariate Gaussian or Normal distribution with marginal means \(\mu_X\) and \(\mu_Y\) along with marginal variances \(\sigma^2_X\) and \(\sigma^2_Y\) and covariance \(\sigma_{XY}\); then \(Z = aX + bY + c\) with constants \(a, b, c\) is Gaussian. If we want to find the mean and variance of \(Z\), we apply the linearity of expectations and variance rules:

\[ \begin{align*} \mathbb{E}(Z) &= \mathbb{E}(aX + bY + c) \\ &= \mathbb{E}(aX) + \mathbb{E}(bY) + \mathbb{E}(c) \\ &= a \mathbb{E}(X) + b \mathbb{E}(Y) + c \\ &= a \mu_X + b \mu_Y + c. \end{align*} \]

\[ \begin{align*} \text{Var}(Z) &= \text{Var}(aX + bY + c) \\ &= \text{Var}(aX) + \text{Var}(bY) + \text{Var}(c) + 2 \text{Cov}(aX, bY) \\ &= a^2 \text{Var}(X) + b^2 \text{Var}(Y) + 0 + 2ab \text{Cov}(X, Y) \\ &= a^2 \sigma_X^2 + b^2 \sigma_Y^2 + 2ab \sigma_{XY}. \end{align*} \]

Important

The same rules apply with more than two Gaussian or Normal random variables. In the case of the variance, the formula will need to include all pairwise covariances.

- Conditional distributions are Gaussian. If \((X, Y)\) have a bivariate Normal or Gaussian distribution with marginal means \(\mu_X\) and \(\mu_Y\) along with marginal variances \(\sigma^2_X\) and \(\sigma^2_Y\) and covariance \(\sigma_{XY}\); then the distribution of \(Y\) given that \(X = x\) is also Gaussian. Its distribution is

\[Y \mid X = x \sim \mathcal{N} \left(\mu_{_{Y \mid X = x}} = \mu_Y + \frac{\sigma_Y}{\sigma_X} \rho_{XY} (x - \mu_X), \sigma^2_{_{Y \mid X = x}} = \ (1 - \rho_{XY}^2)\sigma_Y^2 \right).\]

Here is what is going on here:

- The conditional mean is linear in \(x\) and passes through the mean \((\mu_X, \mu_Y)\), and has a steeper slope with higher correlation.

- The conditional variance is smaller than the marginal variance, and gets smaller with higher correlation.

Here are the conditional means and 90% prediction intervals for the previous plots of bivariate Gaussians with different correlations:

Note

If you want to check the formula for conditional distributions in the general multivariate Normal case, see Petersen & Pedersen’s The Matrix Cookbook, Section 8.1.3 “Conditional Distribution” (it gives the conditional mean and covariance in a partitioned-matrix form).

5 Some Exercises

Consider the multivariate Gaussian distribution of random variables \(X\), \(Y\), and \(Z\) with its respective mean vector

\[\boldsymbol{\mu} = \begin{pmatrix} \mu_X \\ \mu_Y \\ \mu_Z \end{pmatrix} = \begin{pmatrix} 0 \\ 2 \\ 3 \end{pmatrix},\]

correlation matrix

\[ \mathbf{P} = \begin{pmatrix} \rho_{XX} & \rho_{XY} & \rho_{XZ} \\ \rho_{XY} & \rho_{YY} & \rho_{YZ} \\ \rho_{XZ} & \rho_{YZ} & \rho_{ZZ} \end{pmatrix} = \begin{pmatrix} 1 & 0.2 & 0.1 \\ 0.2 & 1 & 0.2 \\ 0.1 & 0.2 & 1 \end{pmatrix}, \]

and marginal variances

\[ \begin{gather*} \sigma_X^2 = 1 \\ \sigma_Y^2 = 1 \\ \sigma_Z^2 = 1. \end{gather*} \]

Now, let us proceed with some exercises.

Exercise A.1

What is the distribution of \(X\)? Select the correct option:

A. \(X \sim \mathcal{N}(\mu_X = 3, \sigma_X^2 = 1)\)

B. \(X \sim \mathcal{N}(\mu_X = 0, \sigma_X^2 = 1)\)

C. \(X \sim \mathcal{N}(\mu_X = 0, \sigma_X^2 = -1)\)

D. \(X \sim \mathcal{N}(\mu_X = 2, \sigma_X^2 = 1)\)

Exercise A.2

What is the joint distribution of \(X\) and \(Z\)? Select the correct option:

A. \(X \sim \mathcal{N}(\mu_X = 1, \sigma_X^2 = 1)\) and \(Z \sim \mathcal{N}(\mu_Z = 3, \sigma_Z^2 = 1)\)

B. Bivariate Gaussian with mean vector \((\mu_X, \mu_Y)^T = (0, 2)^T\), variances \(\sigma_X^2 = 1\) and \(\sigma_Y^2 = 1,\) and \(\rho_{XY} = 0.2\)

C. \(X \sim \mathcal{N}(\mu_X = 1, \sigma_X^2 = 1)\) and \(Y \sim \mathcal{N}(\mu_Y = 2, \sigma_Y^2 = 1)\)

D. Bivariate Gaussian with mean vector \((\mu_X, \mu_Z)^T = (0, 3)^T\), variances \(\sigma_X^2 = 1\) and \(\sigma_Z^2 = 1,\) and \(\rho_{XZ} = 0.1\)

Exercise A.3

What is the distribution of \(Y\), given that \(X = 0.5\)?

Exercise A.4

What is the distribution of \(V = Y - 3X\)?

Exercise A.5

What is \(P(Y < 3X)\)?

5.1 Answers

Solution to Exercise A.1

By property (1) from Section 4.3, it is \(X \sim \mathcal{N}(\mu_X = 0, \sigma_X^2 = 1)\).

Solution to Exercise A.2

By property (1) from Section 4.3, it is bivariate Gaussian with mean vector \((\mu_X, \mu_Z)^T = (0, 3)^T\), variances \(\sigma_X^2 = 1\) and \(\sigma_Z^2 = 1\), and \(\rho_{XZ} = 0.1\).

We just subset the relevant variables by taking the relevant subset of means and variances, and the relevant Pearson correlation.

Solution to Exercise A.3

By property (3) from Section 4.3, it is univariate Gaussian:

\[ \begin{gather*} Y \mid X = 0.5 \sim \mathcal{N} \left(\mu_{_{Y \mid X = 0.5}} = \mu_Y + \frac{\sigma_Y}{\sigma_X}\rho_{XY} (x - \mu_X), \sigma^2_{_{Y \mid X = 0.5}} = \ (1 - \rho_{XY}^2)\sigma_Y^2 \right) \\ Y \mid X = 0.5 \sim \mathcal{N} \left(\mu_{_{Y \mid X = 0.5}} = 2 + \frac{1}{1}(0.2) (0.5 - 0), \sigma^2_{_{Y \mid X = 0.5}} = \ (1 - 0.2^2) 1^2 \right) \\ Y \mid X = 0.5 \sim \mathcal{N} \left( \mu_{_{Y \mid X = 0.5}} = 2.1, \sigma^2_{_{Y \mid X = 0.5}}= 0.96 \right). \end{gather*} \]

Solution to Exercise A.4

By property (2) from Section 4.3, it is univariate Gaussian. We compute the following:

\[ \begin{align*} \mu_V &= \mathbb{E}(V) \\ &= \mathbb{E}(Y - 3X) \\ &= \mu_Y - 3 \mu_X \\ &= 2 - 3(0) = 2 \end{align*} \]

\[ \begin{align*} \sigma^2_V &= \text{Var}(V) \\ &= \sigma_Y^2 + (-3)^2 \sigma_X^2 + 2(-3) \sigma_{XY} \\ &= \sigma_Y^2 + 9 \sigma_X^2 + 2(-3) \rho_{XY} \sigma_X \sigma_Y \\ &= 1 + 9(1) - 6(0.2)(1)(1) \\ &= 8.8. \end{align*} \]

Therefore:

\[ V \sim \mathcal{N}(\mu_V = 2, \sigma^2_V = 8.8). \]

Solution to Exercise A.5

We can use the following:

\[ \begin{align*} P(Y < 3X) &= P(Y - 3X < 0) \\ &= P(V < 0). \end{align*} \]

We already know the distribution of \(V\):

\[ V \sim \mathcal{N}(\mu_V = 2, \sigma^2_V = 8.8). \]

Thus, we use pnorm() as in the below code. Therefore:

\[ P(Y < 3X) = 0.25. \]